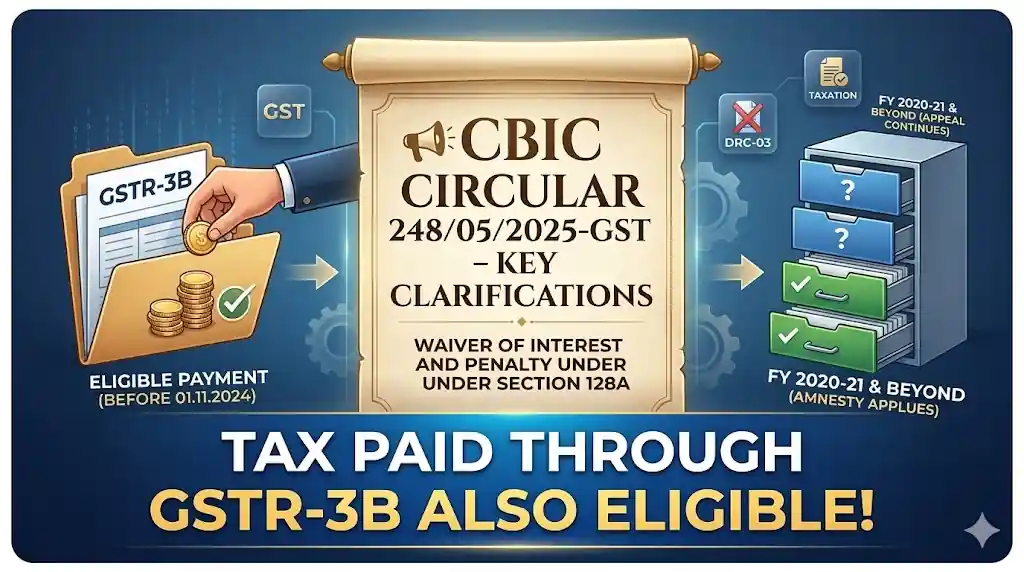

The Central Board of Indirect Taxes and Customs (CBIC) has issued Circular No. 248/05/2025-GST dated 27th March 2025, providing important clarifications on the #GSTAmnestyScheme for waiver of interest and penalty under Section 128A.

🔍 Key Clarifications

1️⃣ Tax Paid Through GSTR-3B Also Eligible

Even if the tax liability was paid through #GSTR3B instead of #DRC03, taxpayers can still avail the amnesty scheme benefit, provided the payment was made before 01.11.2024.

This clarification resolves a major concern for taxpayers who had already discharged their tax liability through the regular return instead of using DRC-03.

2️⃣ Appeals Covering Multiple Periods

Where pending appeals involve multiple tax periods beyond FY 2019-20, the taxpayer can:

✔ Apply for waiver under Section 128A for periods up to FY 2019-20, and

✔ Continue the appeal for periods beyond FY 2019-20, by intimating the appellate authority accordingly.

📌 Why This Matters

These clarifications provide greater flexibility for taxpayers seeking relief under the amnesty scheme, especially in cases involving prior tax payments and multi-period disputes.

Taxpayers and professionals dealing with pending litigation under GST should carefully evaluate these clarifications to optimize the benefits available under Section 128A.

#GST #GSTAmnestyScheme #CBIC #TaxUpdates #GSTLitigation #IndirectTax