The treatment of post-sale discounts and credit notes under GST has always been one of the most debated topics in the history of indirect taxation in India. From the pre-GST regime to the current GST framework, businesses have frequently faced challenges in determining whether discounts should impact the taxable value and input tax credit adjustments.

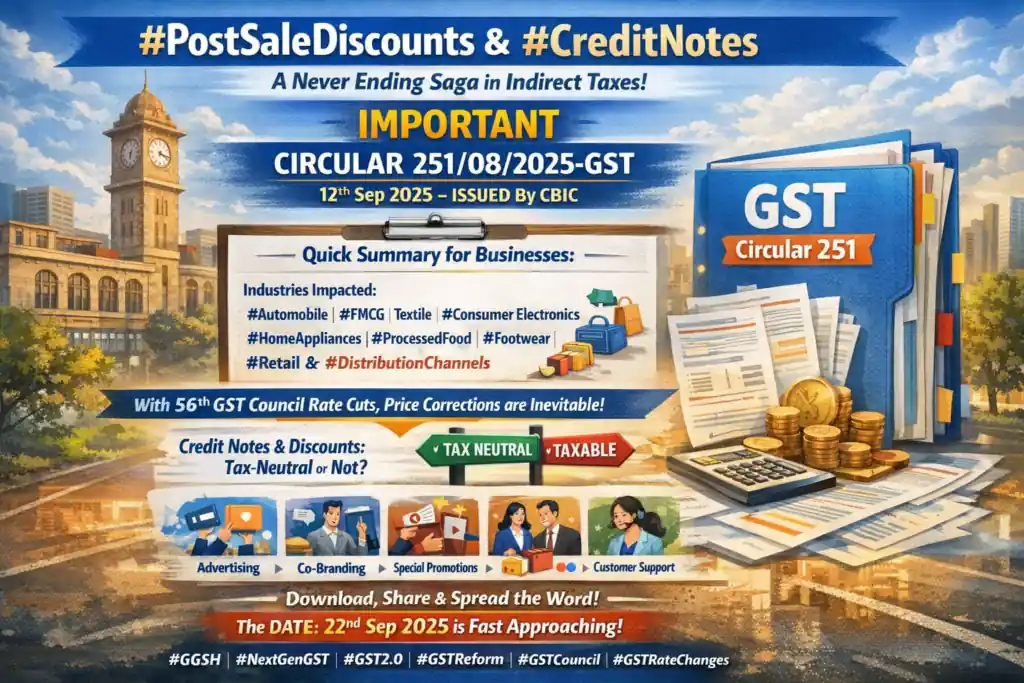

A new clarification has now been issued through GST Circular No. 251/08/2025-GST dated 12 September 2025 by the Central Board of Indirect Taxes and Customs. The circular provides important guidance on the GST treatment of post-sale discounts, incentives, and credit notes, particularly in light of the recent rate rationalisation recommended during the 56th meeting of the GST Council.

For businesses across industries, this circular represents a significant development in understanding when discount-related credit notes remain tax neutral and when they attract GST implications.

Why GST Circular 251 Is Important for Businesses

The recent GST rate changes recommended by the GST Council have led to price adjustments across many sectors. As a result, many companies are expected to issue post-sale discounts or financial adjustments to distributors, dealers, or customers.

This circular helps clarify:

- When credit notes can be issued without affecting GST liability

- When certain incentives or payments are treated as taxable supply of services

- How businesses should structure their sales promotion arrangements

These clarifications are particularly important for companies that regularly provide dealer incentives, promotional discounts, or marketing support payments.

Key Focus of the Circular: Credit Notes and Tax Neutrality

One of the core objectives of the circular is to clarify whether post-sale discounts can reduce the taxable value under GST.

In certain situations, credit notes issued for discounts may remain tax-neutral, meaning they do not trigger additional GST implications.

However, if the payment relates to services provided by the recipient, such as promotional or marketing activities, the transaction may be treated as a taxable supply of services under GST.

This distinction is crucial for businesses that offer performance-based incentives or promotional reimbursements.

Industries Most Impacted by the Circular

Several industries are likely to be affected by the clarifications provided in GST Circular 251/08/2025.

Industries with complex distribution and promotional structures are particularly impacted, including:

- Consumer goods and FMCG companies

- Automobile sector

- Electronics and appliances industry

- Pharmaceutical distribution networks

- Retail and wholesale trading businesses

These sectors often rely on dealer incentives, rebates, marketing reimbursements, and volume discounts, making the new guidance highly relevant.

Sales Promotion Activities That May Require Restructuring

The circular indicates that certain sales promotional arrangements may need restructuring to ensure proper GST compliance.

Examples of promotional activities that may require review include:

- Advertising campaigns conducted by distributors

- Co-branding arrangements

- Product customization services

- Special sales drives and promotional events

- Exhibition or marketing arrangements

- Customer support services provided by channel partners

If these activities are treated as services supplied by the distributor or dealer, GST may become applicable on the consideration received.

Why Businesses Should Review Their Agreements

Many companies structure their dealer incentive schemes and marketing support arrangements through credit notes.

However, if the underlying transaction actually represents consideration for a service, the tax authorities may treat it as a taxable supply rather than a discount.

Businesses should therefore carefully review:

- Distribution agreements

- incentive schemes

- marketing support arrangements

- pricing adjustment mechanisms

A proper review can help avoid future tax disputes, GST demands, or input tax credit complications.

Upcoming Compliance Timeline Businesses Should Note

Businesses should be aware that 22 September 2025 is an important date in relation to the changes discussed in the circular.

Companies must ensure that their commercial arrangements, documentation, and GST treatment of credit notes are aligned with the new clarification before the effective implementation timeline.

Early preparation will help organizations avoid compliance risks and operational disruptions.

Final Thoughts

The clarification issued through GST Circular 251/08/2025-GST marks another important milestone in the evolving interpretation of post-sale discounts and credit notes under the GST framework.

For businesses, this is the right time to:

- Review sales promotion structures

- reassess credit note practices

- align dealer incentive models with GST regulations

Proactive planning will help businesses maintain tax neutrality where possible while avoiding unintended GST liabilities.