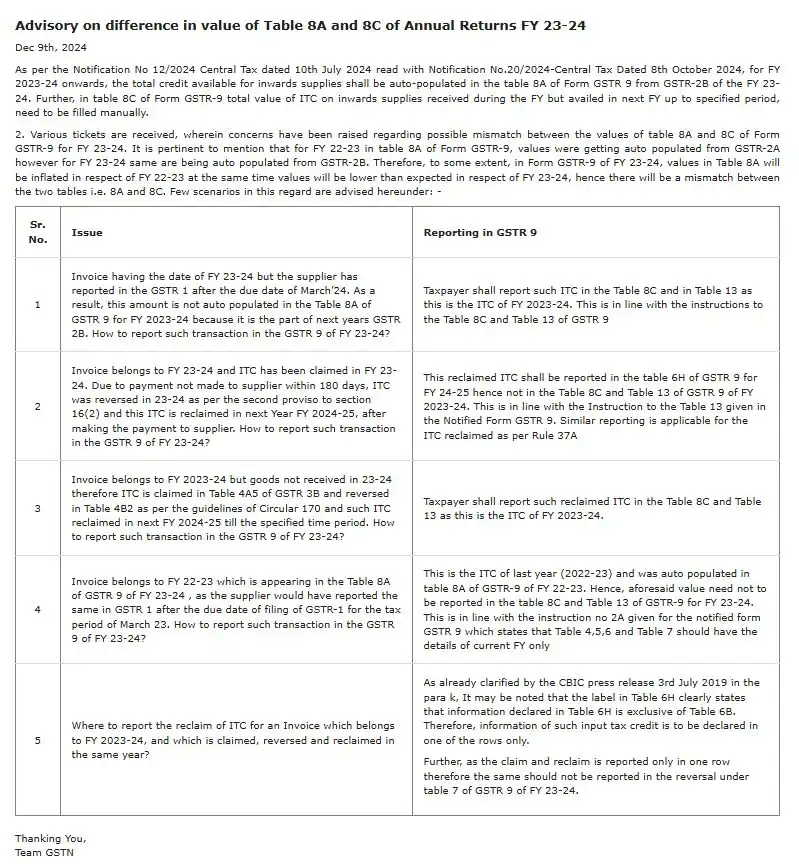

Recent updates in GSTR-9 reporting may lead to differences between Table 8A and Table 8C values for FY 2023-24.

As per Goods and Services Tax Network (GSTN) advisory dated 09-12-2024, changes introduced through Notification No. 12/2024 and Notification No. 20/2024 affect the auto-population of ITC values in the Annual Return.

📌 Key Change

- For FY 2023-24, Table 8A is auto-populated from GSTR-2B.

- For FY 2022-23, it was auto-populated from GSTR-2A.

This shift may result in mismatches between Table 8A and Table 8C while filing GSTR-9.

Reporting Scenarios

1️⃣ Invoice dated FY 2023-24 but reported late by supplier

- ITC should be reported in Table 8C and Table 13 of GSTR-9 for FY 2023-24.

2️⃣ ITC reclaimed in next FY due to late payment to supplier

- Report reclaimed ITC in Table 6H of GSTR-9 for FY 2024-25.

- Do not report in Table 8C or Table 13 of FY 2023-24.

3️⃣ Invoice of FY 2023-24 but goods received in next FY

- Report reclaimed ITC in Table 8C and Table 13 of GSTR-9 for FY 2023-24.

4️⃣ Invoice of FY 2022-23 appearing in Table 8A of FY 2023-24

- Do not report in Table 8C or Table 13 of GSTR-9 for FY 2023-24.

5️⃣ Reclaim of ITC for invoice of FY 2023-24 within the same year

- Report in Table 6H of GSTR-9 for FY 2023-24, not in Table 7.

📊 Takeaway

Due to the shift from GSTR-2A to GSTR-2B for auto-population, taxpayers may notice differences between Table 8A and Table 8C. Proper classification in the relevant tables will help avoid reconciliation issues and compliance errors.

Stay updated. Stay compliant. ✅