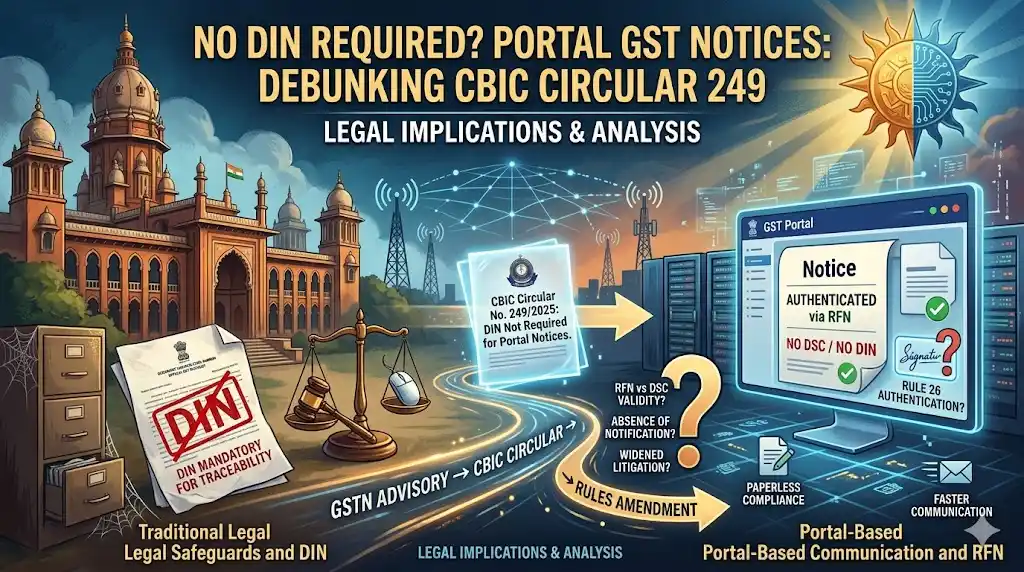

The recent GST Circular No. 249 dated 9th June 2025 issued by the Central Board of Indirect Taxes and Customs (CBIC) has sparked widespread discussion across tax and legal communities.

The headline takeaway making rounds across media platforms is:

“DIN is not required for GST notices issued on the GST portal with RFN.”

While this clarification appears to streamline digital communication under GST, it raises important legal and procedural questions regarding validity, authentication, and compliance with statutory provisions.

Background: GSTN Advisory and Evolution of Digital Notices

This circular builds upon the earlier advisory issued by the Goods and Services Tax Network (GSTN) dated 26th September 2024, which encouraged increased reliance on portal-based communication for GST notices, orders, and reminders.

The broader objective has been to:

- Shift toward paperless GST compliance

- Ensure faster communication with taxpayers

- Improve administrative efficiency

Key Update: DIN Not Required for Portal-Based GST Notices

The CBIC circular clarifies that:

- Document Identification Number (DIN) is not mandatory for notices issued through the GST portal

- Instead, Reference Number (RFN) can be used for authentication

This marks a shift in how official GST communications are validated.

Legal Framework: Section 169 & Rule 26 of CGST Act

To understand the implications, it is crucial to examine:

Section 169 – Mode of Service of Notice

Under the CGST Act, Section 169 provides multiple modes for serving notices, including:

- Direct delivery

- Registered post

- Email communication

- Uploading on the GST portal

However, courts have increasingly scrutinized exclusive reliance on portal uploads.

Rule 26 – Authentication of Documents

Rule 26 mandates that notices and orders must be:

- Signed using Digital Signature Certificate (DSC)

- E-signed as per the Information Technology Act, 2000

- Or verified through any other notified mode of authentication

This brings us to a critical legal question:

Can RFN-based authentication replace DSC or legally notified modes?

Judicial Perspective: Madras High Court’s Stand

The Madras High Court has, in recent rulings, consistently examined the validity of GST notices served through the portal:

Key Cases:

- TVL Dee Dee Creators (02.06.2025)

- M/s Poomika Infra Developers (09.04.2025) – Batch of writ petitions

- M/s Axiom Gen Nxt India Private Limited (22.04.2025) – Larger batch

Key Observations:

- Authorities must ensure proper service of notice

- Mere portal upload may not always suffice

- Taxpayers should not be prejudiced due to procedural lapses

These rulings indicate that procedural compliance remains critical, even in a digital framework.

Critical Issues & Open Questions

The circular raises several important legal and practical concerns:

1. RFN vs DSC Authentication

- Can a system-generated RFN be equated with a digitally signed document?

- Does it meet the legal standards prescribed under Rule 26?

2. Absence of Explicit Notification

- Rule 26 allows “other modes” only if notified by the Board

- Has RFN been formally notified as a valid authentication method?

3. Validity of Notices Without DIN

- DIN ensures traceability and accountability

- Will removing DIN weaken procedural safeguards?

4. Retrospective Validation

- Can future amendments validate past notices retrospectively?

- What happens to already disputed cases?

A Reverse Legal Flow?

An interesting observation in this evolving framework is the perceived sequence:

GSTN Advisory → CBIC Circular → Rules Amendment → Act Amendment → Constitutional Review

This raises questions about whether procedural changes are being regularized after implementation, rather than being legislatively grounded from the outset.

Practical Impact on Taxpayers

For businesses and professionals, this development means:

- Increased reliance on GST portal communications

- Need for regular monitoring of GST portal notices

- Potential legal grounds to challenge improperly authenticated notices

Importantly, taxpayers may still explore:

- Writ remedies before High Courts

- Seeking remand of cases where procedural lapses occurred

Conclusion: Clarity or Continued Litigation?

While the intent behind CBIC Circular No. 249/2025 is to streamline GST communication and address operational gaps, it also opens the door to new legal debates around authentication and validity.

Until there is clear legislative backing or judicial clarity, the issue of DIN vs RFN vs DSC authentication is likely to remain a contested space in GST litigation in India.

Final Thoughts 💬

Is this circular a step toward efficient digital governance, or does it risk procedural dilution in GST law?

Taxpayers, professionals, and legal experts will closely watch how courts interpret these changes in the coming months.