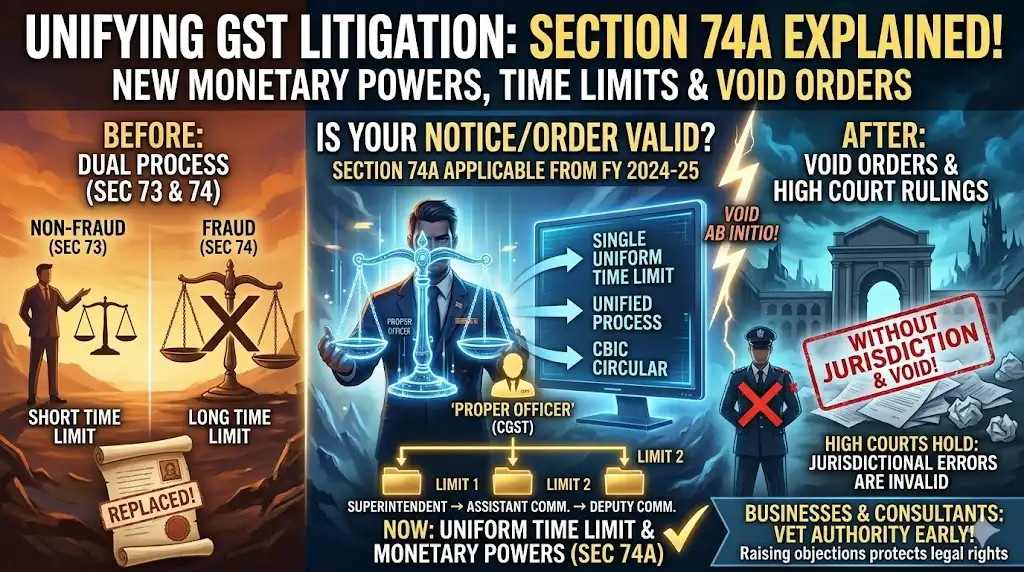

A major transformation has been introduced in the GST assessment and litigation framework with the insertion of Section 74A, applicable from FY 2024-25 onwards.

This new provision replaces the earlier Sections 73 and 74 of the CGST Act and introduces a uniform approach to tax assessments, significantly impacting GST litigation in India.

What is Section 74A in GST?

Section 74A is a newly introduced provision under GST that:

- Replaces Section 73 (non-fraud cases) and Section 74 (fraud cases)

- Introduces uniform time limits for issuing notices and passing orders

- Simplifies the GST assessment process

This marks a shift toward a more streamlined and consistent tax litigation framework.

Key Change: Uniform Time Limit for All Cases

Earlier, GST law differentiated between:

- Fraud cases (longer time limits)

- Non-fraud cases (shorter time limits)

With Section 74A:

👉 A single, uniform time limit now applies to both categories.

Impact:

- Reduces complexity in interpretation

- Brings clarity for taxpayers and tax officers

- Minimizes disputes on limitation

CBIC Circular on Monetary Limits for Officers

The Central Board of Indirect Taxes and Customs (CBIC) has issued a circular prescribing monetary limits for tax officers under Section 74A.

What the Circular Covers:

- Specifies jurisdictional limits for issuing:

- Show Cause Notices (SCN)

- Adjudication orders

- Show Cause Notices (SCN)

- Assigns the “Proper Officer” under:

- Section 74A

- Section 75(2)

- Section 122

- Section 74A

Applicability of Monetary Limits

- These limits currently apply to Central GST officers

- State Governments may:

- Adopt the same limits

- Issue separate circulars for State GST officers

- Adopt the same limits

Legal Consequence: Orders Beyond Power Are Void

One of the most critical aspects of this update is:

⚠️ Any notice or order issued beyond the prescribed monetary limit is without jurisdiction and legally void

This is a crucial safeguard for taxpayers.

Judicial Backing from High Courts

Various High Courts of India have consistently held that:

- Orders passed beyond the authority of officers are invalid

- Jurisdictional errors cannot be cured later

- Such proceedings are liable to be set aside

This principle applies under both:

- Existing GST law

- Earlier indirect tax regimes

What Businesses & Tax Consultants Must Do

With Section 74A in force, it is essential for:

Businesses:

- Review SCNs and orders carefully

- Check whether the issuing officer has proper authority

- Track monetary limits applicable

Tax Consultants:

- Identify jurisdictional errors early

- Raise objections where powers are exceeded

- Advise clients on legal remedies

👉 Awareness is key to protecting your legal rights

Practical Example

If a lower-ranking officer issues:

- A high-value SCN beyond their monetary limit, or

- Passes an order exceeding their jurisdiction

➡️ Such action can be challenged as void ab initio (invalid from the beginning).

Why Section 74A Matters

This reform aims to:

- Bring consistency in GST assessments

- Reduce litigation complexity

- Ensure proper allocation of authority

- Strengthen legal certainty in tax administration

Conclusion

The introduction of Section 74A under GST is a significant step toward a more structured and transparent tax litigation system.

However, with new powers come new responsibilities — both for tax authorities and taxpayers.

Understanding monetary limits and jurisdictional boundaries is now essential to ensure compliance and safeguard legal rights.

Final Thoughts 💬

In GST litigation, knowledge is power.Are you reviewing whether your notices and orders are issued by the right authority within prescribed limits?