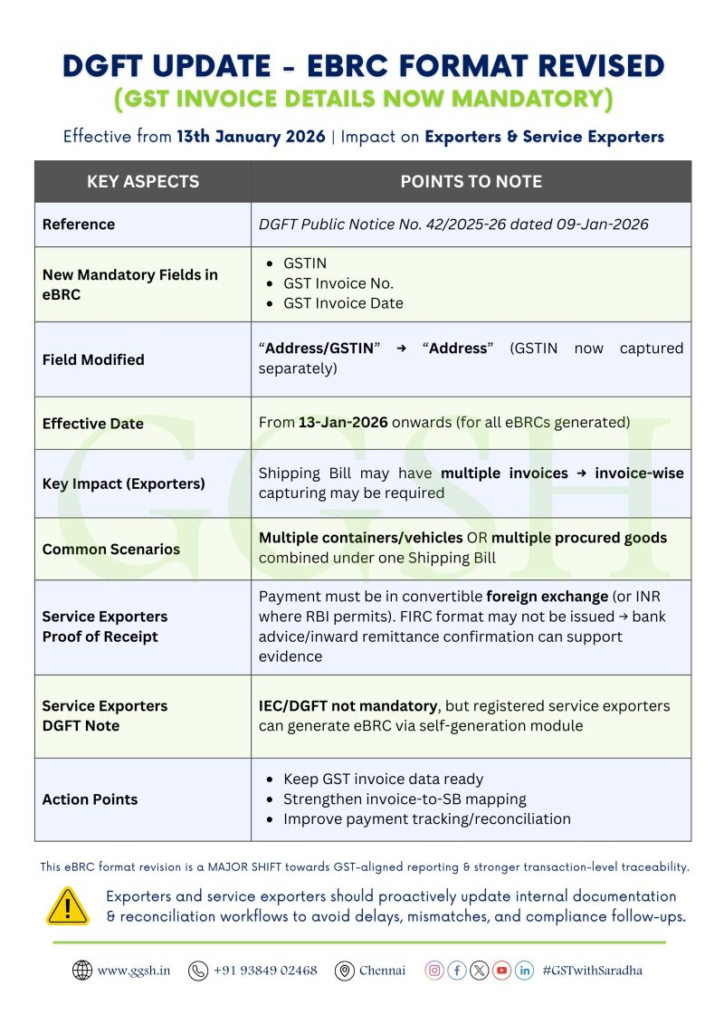

A quiet but impactful change has been introduced by the Directorate General of Foreign Trade (DGFT).

Effective 13th January 2026, the eBRC (Electronic Bank Realisation Certificate) format has been revised—bringing GST into sharper focus by mandating invoice-level reporting.

This move signals a clear shift toward GST-aligned export reporting and enhanced transaction traceability.

What Is eBRC and Why It Matters?

An eBRC is issued by banks to confirm that:

- Export proceeds have been realized in foreign exchange

- The transaction qualifies for export benefits under DGFT schemes

👉 It plays a crucial role in:

- Claiming export incentives

- Proving realization of export proceeds

- Ensuring regulatory compliance

What’s New in the Revised eBRC Format?

From January 2026 onwards, the following details are mandatory in eBRC:

📌 Newly Required Fields:

- GSTIN

- GST Invoice Number

- GST Invoice Date

👉 This transforms eBRC from a summary-level document to a more granular, invoice-linked record.

The Big Shift: Invoice-Level Traceability

The revised format introduces a fundamental change:

👉 One Shipping Bill ≠ One Invoice anymore (for reporting purposes)

Instead:

- A single shipping bill may include multiple invoices

- Each invoice must now be:

- Identified

- Tracked

- Reported accurately

- Identified

Practical Challenges Exporters Will Face

1. Complex Invoice-to-Shipping Bill Mapping

Situations where complexity increases:

- Multiple invoices under one shipping bill

- Multiple containers or transport modes

- Clubbing of goods from different procurements

👉 Manual tracking systems may no longer be sufficient.

2. Payment Tracking & Reconciliation

Export proceeds may be:

- Received in parts

- Adjusted across invoices

- Linked to multiple shipments

👉 Matching payments with specific GST invoices becomes critical.

3. Service Exporters – Documentation Pressure

For service exporters:

- FIRC (Foreign Inward Remittance Certificate) may not always be issued

- Alternative bank documents are used

👉 Now, linking such receipts with GST invoices becomes even more important.

Why This Change Matters

This update is not just procedural—it reflects a broader regulatory intent:

🔍 Stronger Data Integration

- Alignment between GST filings and DGFT records

🔍 Improved Traceability

- Invoice-level audit trail

🔍 Reduced Misreporting

- Better validation of export transactions

Action Points for Exporters

Before generating your next eBRC, ensure the following:

✔️ Keep GST Invoice Data Ready

- GSTIN

- Invoice number & date

- Accurate invoice classification

✔️ Strengthen Invoice-to-Shipping Bill Mapping

- Maintain clear linkage between:

- Invoices

- Shipping bills

- Export documentation

- Invoices

✔️ Improve Payment Tracking Systems

- Track receipts invoice-wise

- Reconcile bank realization with GST data

✔️ Upgrade Internal Processes

- Move from summary-level tracking to transaction-level control

- Use ERP or structured reconciliation tools where possible

Impact on Compliance & Risk

Failure to adapt may lead to:

- Delays in eBRC generation

- Issues in claiming export benefits

- Mismatches during audits

- Increased compliance scrutiny

Conclusion

The revised eBRC format introduced by the Directorate General of Foreign Trade marks a significant step toward data-driven export compliance.

While the change may appear minor, its impact on documentation, reconciliation, and reporting discipline is substantial.

Final Thought 💬

In the new compliance landscape, it’s no longer enough to prove that exports happened.👉 You must now prove it invoice by invoice, transaction by transaction.