“Every new institution speaks through its first order.”

On 11th February 2026, the Goods and Services Tax Appellate Tribunal (GSTAT), Principal Bench, Delhi delivered its first-ever second appeal decision in:

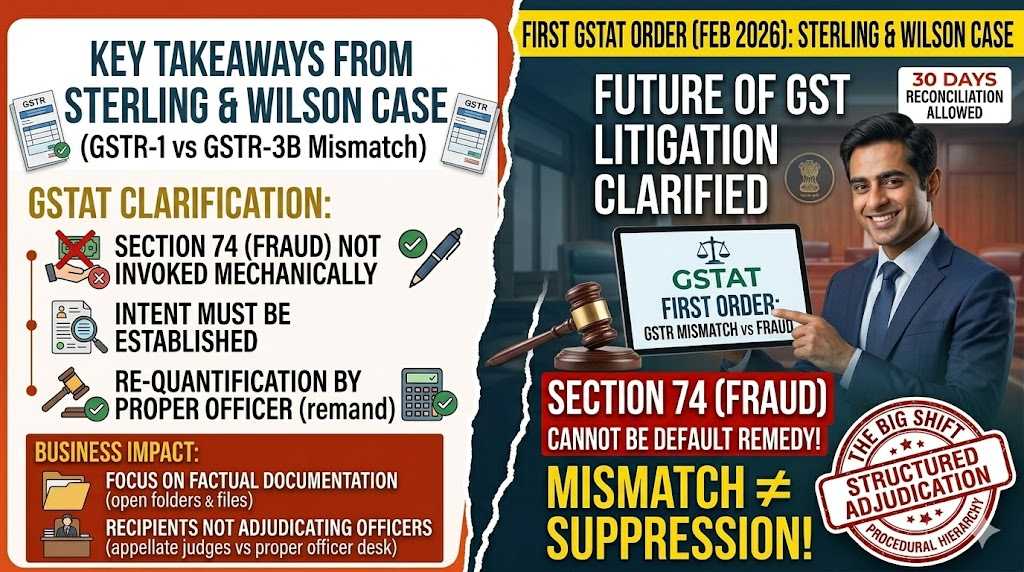

M/s Sterling & Wilson Pvt. Ltd. vs Commissioner, Odisha CT GST & Ors.

At first glance, the issue may seem routine—a GSTR-1 vs GSTR-3B mismatch for FY 2018–19.

But that is precisely why this order matters.

Case Background: A Common Issue, A Crucial Clarification

The dispute involved:

- Mismatch between GSTR-1 and GSTR-3B

- Proceedings initiated under Section 74 (fraud/suppression)

However:

- At the appellate stage, fraud allegations were not sustained

Key Ruling by GSTAT

The Goods and Services Tax Appellate Tribunal made a critical clarification:

👉 If fraud or suppression is not established, the case must be re-determined under Section 73

And importantly:

👉 The matter must go back to the Proper Officer for fresh adjudication

Why This Matters

1. Clear Separation Between Section 73 & 74

- Section 74 → Requires intent (fraud/suppression)

- Section 73 → Applies to non-fraud cases

👉 The ruling reinforces that Section 74 cannot be invoked mechanically.

2. Appellate Forums Have Defined Limits

The Tribunal emphasized:

👉 Appellate authorities cannot step into the shoes of adjudicating officers to re-quantify tax demands

Instead:

- They must remand the matter for proper determination

3. Recognition of Early GST Challenges

A notable aspect of the order is its practical approach:

- Acknowledgement of:

- Initial GST implementation issues

- Portal limitations

- Manual filings

- COVID-19 disruptions

- Initial GST implementation issues

👉 The Tribunal allowed the taxpayer:

- 30 days to reconcile and amend records

Key Takeaways for Businesses & Professionals

✔️ Section 74 Cannot Be Used by Default

- Fraud must be:

- Clearly alleged

- Properly established

- Clearly alleged

✔️ Mismatch ≠ Suppression

- Differences between returns do not automatically imply intent to evade

✔️ Right Forum, Right Process Matters

- Adjudication → Appeal → Tribunal

- Each stage has a defined role

✔️ Remand Is Not a Setback

- It provides:

- Opportunity to correct errors

- Chance for proper reconciliation

- Opportunity to correct errors

What This First GSTAT Order Signals

This decision sets the tone for how GSTAT may function going forward:

🔹 Fact + Law Driven Approach

- Not just legal interpretation, but factual examination

🔹 Balanced View on Compliance Gaps

- Distinguishing genuine errors from deliberate non-compliance

🔹 Structured Adjudication

- Preference for proper re-determination over penalties

Impact on GST Litigation Strategy

For taxpayers and professionals, this order is an early indicator:

👉 Litigation strategy must focus on:

- Correct classification (Section 73 vs 74)

- Strong factual documentation

- Proper sequencing of appeals

Conclusion

The first order of the Goods and Services Tax Appellate Tribunal is not just about a GSTR mismatch.

It is about:

👉 Discipline in invoking provisions

👉 Respect for procedural hierarchy

👉 Fair treatment of genuine compliance gaps

Final Thought 💬

In GST litigation, the real question is not just:

“Is there a mismatch?”

But:

“Does it justify intent?”