A practitioner’s note on the apparent conflict between the Andhra Pradesh High Court and the Calcutta High Court on the power of a transit-state officer to intercept and detain goods.

The Promise & The Present Reality

In 2017, GST was sold to industry on a single, powerful idea – the seamless movement of goods across India. One nation, one tax, no check-posts at every border. Nearly nine years on, businesses still find themselves litigating a surprisingly basic question: can goods be intercepted, detained or confiscated by any officer, anywhere in the country, simply because the vehicle happened to pass through that State?

On the ground, the answer often feels like “yes”. On the statute book and in recent case law, the position is far less settled. Two recent High Court decisions have, in fact, answered the very same question in opposite ways – and the divergence is instructive for anyone who advises on movement of goods.

The Two Rulings

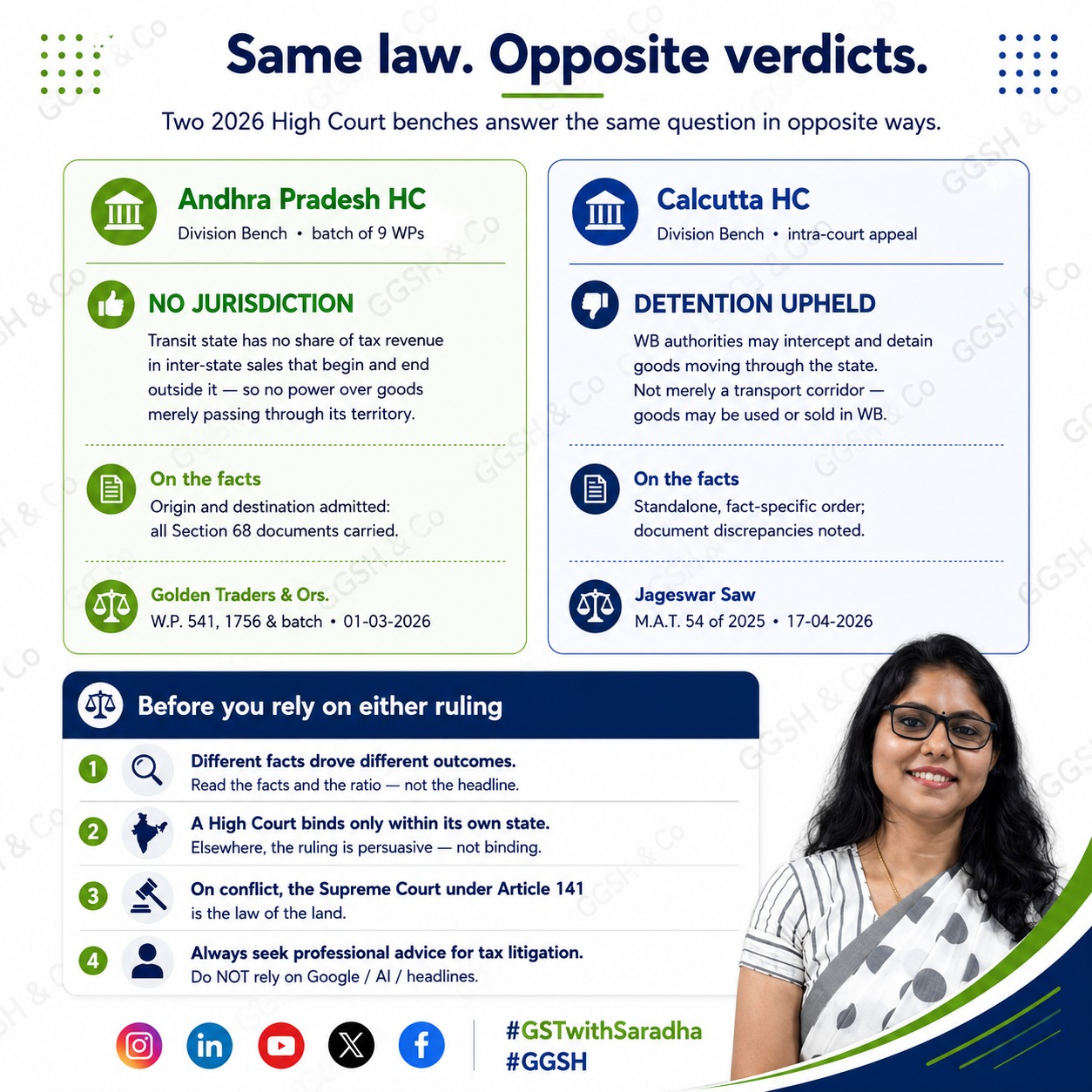

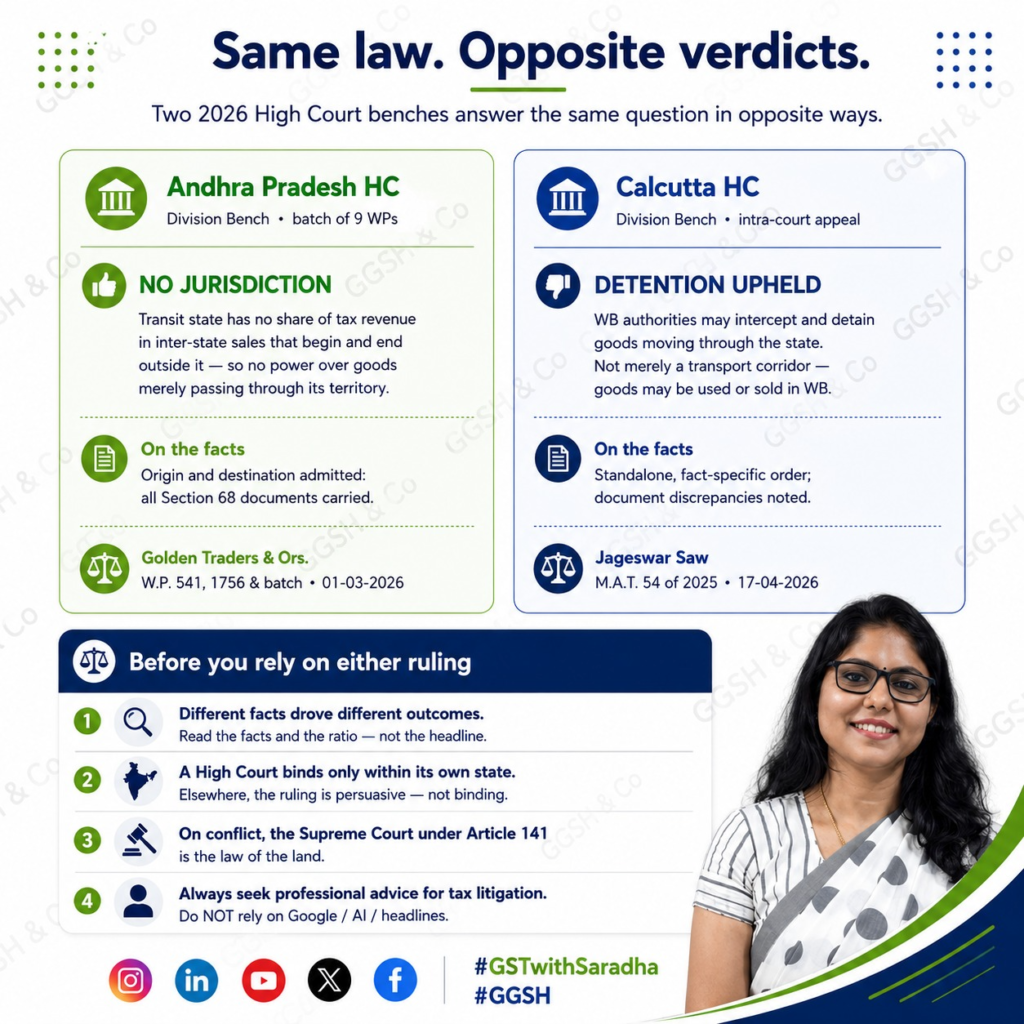

Andhra Pradesh High Court (Division Bench) – Golden Traders – W.P. Nos. 541, 1756, 3097, 3225, 3227, 3252, 3254, 3258 & 3354 of 2026, dated 01-03-2026.

The Division Bench took the view that a transit State has no share of tax revenue in an inter-State sale that originates outside the State and culminates outside the State. Since the transit State has no fiscal stake in such a transaction, it has no jurisdiction over goods that merely pass through its territory en route to another State.

Calcutta High Court — Jageswar Saw, M.A.T. 54 of 2025, dated 17-04-2026.

Hearing an appeal against an order of the Single Judge, the Division Bench took the opposite view and upheld the power of the West Bengal authorities to intercept and detain goods moving through the State.

Same GST law. Similar movement of goods. Very different judicial outcomes. So how does one reconcile them?

Why the outcomes diverged: read the FACTS, not the headline

The instinct is to treat these as two benches taking diametrically opposite views of the same legal question. A closer reading suggests the divergence is driven by a thin but decisive line of fact.

The Calcutta decision is a standalone, fact-specific order. The Court flagged a lack of clarity in the facts before it. In Para 32, the Bench observed that on the material on record, “it cannot be accepted that West Bengal was merely a transport corridor and the goods would not be used or sold in West Bengal.” The order also records discrepancies in the accompanying documents. In other words, the Court was not satisfied that West Bengal was a pure pass-through State, and it was not dealing with clean documentation.

The Andhra Pradesh decision arises in a very different posture. It is a batch order disposing of nine petitions on common facts. The judgment proceeds on concluded facts as to the origin State and the destination State (Para 4) and on an admitted position that the goods were accompanied by all the documents required under Section 68 (Para 5). On those facts, Andhra Pradesh genuinely was only a transit corridor, and the documentation was not in question.

That single distinction does a great deal of work:

- In Andhra Pradesh, the State’s status as a mere transit corridor and the sufficiency of Section 68 documentation were settled. The Court could therefore reach the jurisdictional question cleanly.

- In Calcutta, neither of those things was established. The transit-corridor claim was contested, and the documents were deficient. The Court never had to decide the pure jurisdictional question on undisputed facts.

So while the two orders appear to be on the same subject, the divergence is at least as much a function of facts and circumstances as of any irreconcilable view of law. That differentiation is critical before either order is cited as authority.

The precedent question: binding versus persuasive, and Article 141

Even where two High Courts do genuinely differ on a question of law, a practitioner cannot simply pick the favourable one. Two settled principles govern how these orders may be used:

A High Court judgment is binding only within its own territorial jurisdiction. The Andhra Pradesh order binds authorities and tribunals within Andhra Pradesh; the Calcutta order binds within West Bengal. Outside its home State, a High Court ruling carries persuasive value – it can be cited and relied upon as reasoning – but it is not binding precedent.

When conflicting views emerge, the Supreme Court settles the law. A reasoned judgment of the Supreme Court on the merits becomes, by virtue of Article 141 of the Constitution, the law of the land binding on all courts within the territory of India. Until and unless the issue is taken up and decided by the Supreme Court, taxpayers across different States may continue to face genuinely different positions depending on where the vehicle is stopped.

What this means for businesses and advisers

For a transporter or consignor whose goods are detained in a transit State, the practical lesson is not “the Andhra Pradesh order protects me everywhere.” It does not. The lesson is more disciplined:

- Establish the FACTS FIRST. Is the State of detention genuinely only a transit corridor – origin and destination both elsewhere? Are the Section 68 documents complete and consistent? The strength of any jurisdictional argument rises and falls on these facts.

- Match the facts before citing the case. A favourable order helps only where your facts mirror it. Andhra Pradesh helps the clean transit, complete documents fact pattern. Calcutta is a caution for the contested corridor, deficient documents fact pattern.

- Know your forum. Within your own State, the local High Court position governs. Elsewhere, you are arguing on persuasive value and on first principles, not on binding precedent.

- Watch for escalation. Given the split, this is precisely the kind of issue that may ultimately need an authoritative Supreme Court ruling under Article 141. Track the position rather than treating any single headline as final.

A Closing Caution

Headlines, search engines and AI summaries are tempting shortcuts in tax practice, and an apparent “conflict” between two High Courts makes for striking copy. But the discipline of the profession lies in reading the issue, the facts and the ratio and in recognising when a divergence is genuinely about law and when it is, on closer reading, about facts.

Before relying on either of these orders, study the full text, map it against your own fact pattern, and seek professional advice rather than drawing quick conclusions from matching case titles.

This article is intended as general information for tax professionals and does not constitute legal or professional advice. Citations should be independently verified against the certified copies of the orders, and the full text of each judgment should be read before reliance.