Purchasing goods or services from unregistered vendors is common in many businesses.

On paper, these transactions may appear simple. However, under the Goods and Services Tax (GST) framework, procurement from Unregistered Persons (URPs) can quietly introduce significant compliance obligations and tax risks.

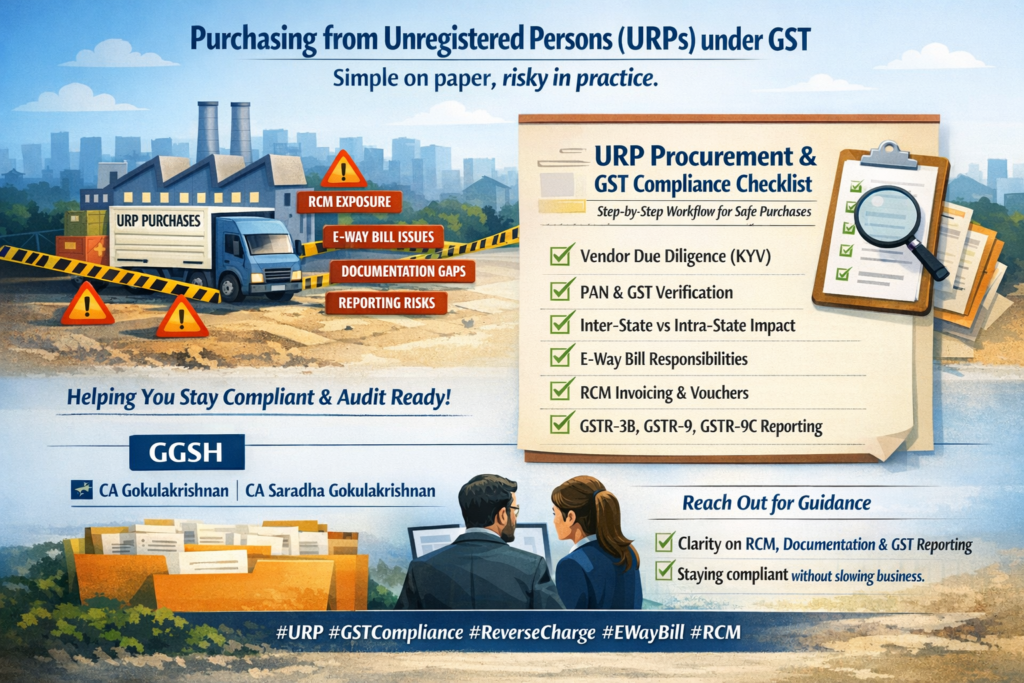

What many businesses treat as routine procurement can trigger issues such as:

- Reverse Charge Mechanism (RCM) exposure

- E-way bill compliance responsibilities

- Self-invoicing documentation gaps

- Return reporting inconsistencies

- Audit risks during GST scrutiny

As URP transactions increase in volume, these compliance gaps often surface only during GST audits or departmental reviews.

To address this, our team has developed a Practical URP Procurement & GST Compliance Checklist designed to help procurement teams, finance professionals, and compliance officers manage URP transactions systematically.

What is a URP under GST?

A URP (Unregistered Person) refers to a supplier who is not registered under GST.

When a registered business procures goods or services from such vendors, certain transactions may attract the Reverse Charge Mechanism (RCM).

Under RCM, the tax liability shifts from the supplier to the recipient, meaning the buyer must:

- Pay GST directly to the government

- Issue self-invoices for the transaction

- Report the liability in GST returns

This is where compliance complexity begins.

Why URP Purchases Can Become Risky

Many organisations assume URP procurement is administratively easier because the supplier does not charge GST.

However, in practice these transactions introduce hidden compliance layers.

Common risks in URP transactions

1. Reverse Charge liability not identified

Certain categories of URP purchases automatically trigger RCM.

2. Missing self-invoices and payment vouchers

Under GST law, the recipient must generate these documents for URP purchases.

3. E-way bill confusion

When the supplier is unregistered, the responsibility for generating the e-way bill may shift to the recipient.

4. Incorrect GST return reporting

RCM liabilities must be properly reported in GSTR-3B and annual returns.

5. Documentation gaps during audit

Poor record management can create issues during GST assessments and departmental audits.

Practical URP Procurement & GST Compliance Checklist

To help businesses manage URP transactions properly, we recommend implementing a structured compliance workflow covering the following steps.

1. Vendor Due Diligence (KYV – Know Your Vendor)

Before onboarding any unregistered supplier, businesses should perform basic vendor verification.

Recommended checks include:

- Identity verification of the supplier

- Address validation

- Nature of business activity

- Transaction history and credibility

A KYV framework helps reduce compliance risk and strengthens procurement governance.

2. PAN and GST Registration Status Verification

Always verify whether the supplier is actually unregistered.

Important checks include:

- PAN verification

- GST registration status on the GST portal

- Confirming whether the supplier falls under mandatory registration thresholds

Sometimes suppliers claim URP status even when they are legally required to register under GST.

3. Inter-State vs Intra-State Transaction Analysis

URP transactions must be evaluated for location-based tax implications.

Businesses should determine:

- Whether the transaction is inter-state or intra-state

- Whether the supply triggers IGST or CGST/SGST liability

- Whether additional compliance obligations arise

Correct classification is critical for accurate GST return reporting.

4. E-Way Bill Responsibility

When the supplier is unregistered, the responsibility for generating an e-way bill may fall on the recipient.

Businesses must verify:

- Whether the consignment value exceeds the e-way bill threshold

- Who is responsible for generating the e-way bill

- Whether transporter details are properly documented

Failure to comply can result in movement-related penalties under GST law.

5. Self-Invoice and Payment Voucher Requirements

For URP purchases subject to RCM, businesses must generate:

- Self-invoice for the supply

- Payment voucher at the time of payment

These documents must be issued within the timelines prescribed under GST law.

Failure to maintain these records is a common audit observation.

6. GST Return Reporting

URP transactions subject to RCM must be properly disclosed in GST returns, including:

- GSTR-3B

- Annual Return (GSTR-9)

- GST Reconciliation Statement (GSTR-9C)

Incorrect classification or omission can create mismatches during GST reconciliation.

7. Record Retention and Audit Readiness

Businesses should maintain structured documentation for URP transactions, including:

- Vendor verification records

- Self-invoices and payment vouchers

- Transport documents and e-way bills

- GST return reporting support documents

Proper documentation ensures smooth GST audits and departmental inspections.

Why Procurement and Finance Teams Must Work Together

URP transactions often originate from procurement teams, while GST compliance is handled by finance departments.

Without coordination, gaps can easily arise.

A structured checklist ensures:

- Procurement teams ask the right questions upfront

- Finance teams receive complete documentation

- Compliance risks are identified before audits begin

The Goal: Compliance Without Slowing Business

The purpose of a URP procurement checklist is not to create additional bureaucracy.

Instead, it helps businesses:

- Identify RCM exposure early

- Avoid downstream GST disputes

- Ensure accurate return reporting

- Stay compliant without disrupting procurement operations

When implemented properly, a structured workflow protects businesses from avoidable GST risks while maintaining operational efficiency.

Final Thoughts

Purchases from Unregistered Persons (URPs) are a regular part of business operations across industries.

But under GST, these transactions carry hidden compliance responsibilities.

With proper vendor verification, documentation discipline, and return reporting controls, businesses can manage URP procurement efficiently while remaining fully compliant.A practical compliance checklist ensures that URP transactions remain routine procurement — not a future audit risk.