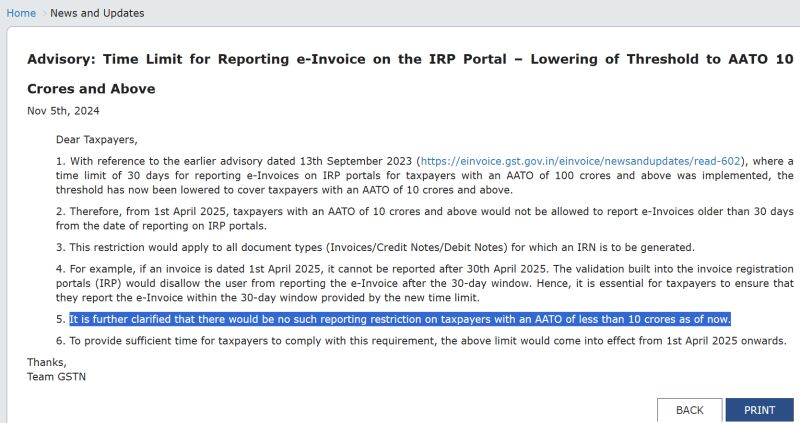

A significant update in the GST e-invoicing framework will impact businesses with higher turnover starting 1 April 2025. As per the latest advisory from the Goods and Services Tax Network, the 30-day time limit for reporting invoices to the e-invoice portal will now apply to taxpayers with Annual Aggregate Turnover (AATO) above ₹10 crore, replacing the earlier threshold of ₹100 crore.

This change is aimed at improving real-time invoice reporting, tax compliance, and transparency in GST transactions. At the same time, the advisory also clarifies an important point for smaller taxpayers.

What is the 30-Day Time Limit for E-Invoice Reporting?

Under the GST e-invoicing system, eligible taxpayers must upload invoice details to the Invoice Registration Portal (IRP) to generate an Invoice Reference Number (IRN).

Previously:

- The 30-day reporting restriction applied only to taxpayers with AATO above ₹100 crore.

Now, from 1 April 2025, the rule will apply to taxpayers with:

- Annual Aggregate Turnover above ₹10 crore

This means such businesses must report invoices to the IRP within 30 days of the invoice date. After this period, the invoice cannot be reported or validated on the e-invoice portal, which may create compliance issues.

No Reporting Restriction for Businesses Below ₹10 Crore

A key clarification in the advisory is that taxpayers with an AATO below ₹10 crore currently have no such reporting time restriction.

This means:

- There is no 30-day limit for e-invoice reporting for businesses below ₹10 crore turnover.

- They can generate e-invoices without the system blocking reporting based on the invoice date.

This clarification is important because many compliance disputes have arisen in the past due to misunderstandings around the absence of a reporting time limit.

Impact on GST Compliance and Business Operations

The reduction of the threshold from ₹100 crore to ₹10 crore turnover will significantly increase the number of businesses affected by the 30-day e-invoice reporting requirement.

Businesses should prepare for:

- Stronger internal invoice reporting controls

- Timely uploading of invoices to the IRP

- Better coordination between accounting teams and ERP systems

- Monitoring of invoice dates and IRN generation timelines

Failure to comply may lead to inability to generate valid e-invoices, which can impact GST return filing, input tax credit claims, and compliance verification during audits.

E-Invoice Absence and Goods Detention under Section 129

One of the practical issues faced by businesses relates to detention of goods during transit due to absence of e-invoice or IRN, often invoked under **Central Goods and Services Tax Act, 2017 Section 129.

In several cases, tax officers have detained goods when e-invoices were not generated at the time of transportation, especially for taxpayers with turnover below ₹100 crore.

However, taxpayers often argued that:

- The GST advisory allowed 30 days for reporting invoices, or

- No time restriction existed for taxpayers below the specified threshold

This led to conflicting interpretations between taxpayers and enforcement authorities.

Does the New Advisory Provide Relief?

The updated advisory provides greater clarity by explicitly stating that taxpayers with turnover below ₹10 crore currently have no reporting restriction.

This clarification may help strengthen the argument that:

- Absence of e-invoice within a specific timeframe cannot automatically be treated as non-compliance for such taxpayers.

- Detention of goods purely on this ground may require careful legal interpretation and justification.

While the advisory does not directly amend enforcement provisions, it reduces ambiguity surrounding the reporting time limit.

What Businesses Should Do Before April 2025

Businesses with turnover above ₹10 crore should start preparing now to comply with the upcoming rule.

Recommended steps include:

✔ Updating ERP and accounting systems to ensure timely e-invoice generation

✔ Monitoring invoice reporting timelines to avoid delays beyond 30 days

✔ Training accounting teams on the revised e-invoice compliance rules

✔ Reviewing logistics documentation to avoid transit issues

Early preparation will help businesses avoid system blocks, compliance risks, and operational disruptions.

Conclusion

The GST advisory reducing the 30-day e-invoice reporting threshold from ₹100 crore to ₹10 crore turnover marks a significant expansion of the e-invoicing compliance framework.

While the change increases compliance obligations for many businesses, it also brings an important clarification: taxpayers with turnover below ₹10 crore currently have no reporting time restriction.As the new rule becomes effective from 1 April 2025, businesses should review their invoice reporting processes and GST compliance systems to ensure smooth implementation and avoid potential disputes.