“Can we go directly to High Court?”

“Can we avoid pre-deposit through a writ petition?”

These are among the most common questions in GST litigation strategy.

But here’s the reality:

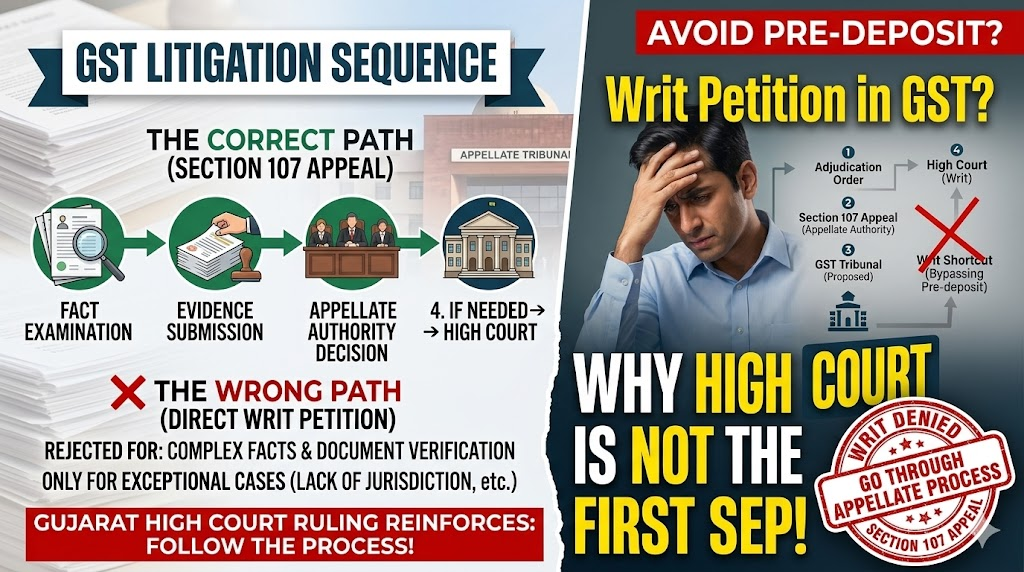

👉 A writ petition is an exception—not the default remedy.

A recent ruling by the Gujarat High Court reinforces this principle with clarity, especially in cases involving Input Tax Credit (ITC) disputes.

Case Background: ITC Denial & Direct Writ Approach

In this case:

- ITC was denied under Section 16(2)(c) of GST law

- The taxpayer approached the High Court directly

- Grounds raised included:

- Constitutional validity

- Alleged violation of natural justice

- Constitutional validity

At first glance, these seem like strong reasons to invoke writ jurisdiction.

But the Court chose a different approach.

Court’s Stand: Process Before Protest

Instead of examining the merits of ITC eligibility, the Gujarat High Court focused on a more fundamental question:

👉 Was the correct legal process followed?

The Court observed:

- The dispute involved:

- Examination of facts

- Verification of documents

- Assessment of supplier conduct

- Examination of facts

👉 These are matters best handled through the statutory appellate mechanism, not writ jurisdiction.

Section 107 Appeal: Not Just a Formality

Under GST law:

- Section 107 provides the right to appeal against orders

- It includes:

- Detailed fact examination

- Opportunity for evidence submission

- Structured adjudication

- Detailed fact examination

The Court emphasized:

👉 This appellate route is not optional—it is the correct first step in most cases.

When Can a Writ Petition Be Filed?

Writ jurisdiction is meant for exceptional situations, such as:

✔️ Lack of Jurisdiction

- Authority acted beyond legal powers

✔️ Violation of Natural Justice

- No hearing given

- Bias or procedural unfairness

✔️ Constitutional Challenges

- Validity of law itself is questioned

✔️ Patent Legal Errors

- Clear, undisputed legal mistakes

👉 Even in such cases, courts exercise caution.

Why Courts Discourage Direct Writs in GST Matters

The reasoning is practical:

- GST disputes often involve complex facts

- Require document verification

- Need technical analysis

High Courts are not designed to function as fact-finding authorities in the first instance.

Key Takeaways for GST Litigation Strategy

1. Two Critical Decisions in Every Dispute

Every GST case involves:

👉 WHAT to challenge (legal issue)

👉 HOW to challenge (correct forum & process)

Both are equally important.

2. Avoid Using Writ as a Shortcut

- Filing a writ to bypass:

- Pre-deposit

- Appellate procedures

- Pre-deposit

…may backfire.

👉 Courts may simply redirect you to the proper forum.

3. Respect the Litigation Sequence

- Adjudication → Appeal → Higher forums

👉 Skipping steps weakens your position.

4. Build Your Case at the Right Stage

- Appellate authorities allow:

- Evidence submission

- Detailed arguments

- Fact-based defense

- Evidence submission

👉 This foundation is crucial for future litigation.

Practical Advice for Businesses & Professionals

✔️ Before Filing a Writ

- Ask:

- Is this truly an exceptional case?

- Are facts disputed?

- Is evidence evaluation required?

- Is this truly an exceptional case?

✔️ Prefer Appeal Route When:

- ITC eligibility is in question

- Supplier compliance is involved

- Documentation needs scrutiny

✔️ Use Writ Strategically

- Only when:

- Legal error is clear

- Process is fundamentally flawed

- Legal error is clear

Conclusion

The ruling by the Gujarat High Court serves as an important reminder:

👉 Writ jurisdiction is not a shortcut—it is a safeguard.

In GST litigation, success is not just about legal strength, but also about:

- Proper sequencing

- Forum selection

- Strategic restraint

Final Thought 💬

In every GST dispute, the real question is not just:

“Can we go to High Court?”

But:

“Should we go there now—or later?”