Taxpayers filing the October 2024 GSTR-3B return should exercise extra caution while claiming Input Tax Credit (ITC) based on GSTR-2B. Several professionals have reported instances where ITC already reflected in the September 2024 GSTR-2B is again appearing in the October 2024 GSTR-2B, potentially leading to duplicate ITC claims.

This issue appears to be linked to the Invoice Management System (IMS) and the reporting timeline for QRMP suppliers and Input Service Distributor (ISD) returns.

Businesses must therefore ensure proper ITC reconciliation before filing GSTR-3B to avoid errors, notices, or future reversals.

Why Duplicate ITC Is Appearing in GSTR-2B

The duplication issue mainly arises due to the filing timelines of QRMP suppliers and ISD registrations.

Under the GST framework:

- QRMP taxpayers file GSTR-1 quarterly

- ISD registrations file GSTR-6

- The cut-off date for capturing these transactions in GSTR-2B is typically the 13th of the month

If a QRMP supplier files GSTR-1 for September 2024 on 12th or 13th October, or an ISD files GSTR-6 during this window, the credit may have already appeared in the September 2024 GSTR-2B.

However, due to a possible algorithm or synchronization issue within the IMS system, the same ITC is again reflecting in the October 2024 GSTR-2B.

This creates a risk where taxpayers relying solely on GSTR-2B may accidentally claim duplicate ITC while filing GSTR-3B for October 2024.

Role of IMS in GSTR-2B Data Flow

The Invoice Management System (IMS) introduced by the Goods and Services Tax Network is designed to streamline invoice-level matching and ITC validation.

However, during the initial phase of IMS implementation, certain data synchronization and reporting challenges appear to be affecting how credits are captured in GSTR-2B.

Because GSTR-2B is now influenced by IMS data flows, any discrepancies in the system may result in incorrect or duplicated ITC values being auto-populated in GSTR-3B.

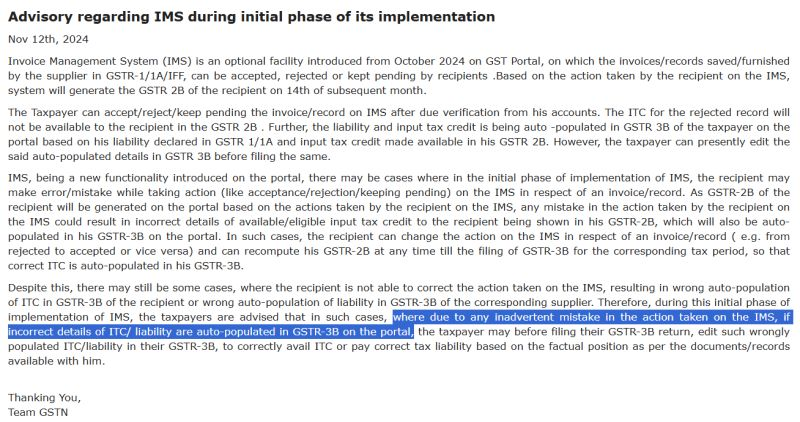

GSTN Advisory on IMS and ITC Reporting

Earlier, the Goods and Services Tax Network had issued an advisory in November explaining that if incorrect ITC or liability values appear auto-populated in GSTR-3B, taxpayers should carefully review and edit the figures before filing the return.

The advisory highlighted that such discrepancies could arise due to inadvertent actions in IMS.

However, many professionals believe that some of the current issues may also stem from system-level glitches during the early stages of IMS implementation.

Action Points for Taxpayers Filing October 2024 GSTR-3B

To avoid compliance issues or duplicate credit claims, taxpayers should follow these important steps before filing their return.

1. Do Not Claim ITC Solely Based on GSTR-2B

While GSTR-2B is an important reference document, ITC claims should not be made solely based on the auto-populated values.

2. Validate ITC with Purchase Records

Taxpayers should reconcile GSTR-2B with purchase registers, invoices, and earlier month credits to ensure accuracy.

3. Check for Duplicate Credits

Special attention should be given to credits from QRMP suppliers and ISD registrations, especially if they were filed around the 12th or 13th of October 2024.

4. Ensure Accurate ITC Calculation

Before filing GSTR-3B, verify that the ITC claimed is correct and does not include duplicate entries.

5. Raise a Grievance if Required

If duplicate credits continue to appear due to system issues, taxpayers may consider raising a grievance through the GST portal for clarification or correction.

Importance of Careful ITC Reconciliation

Claiming incorrect or excess ITC can lead to:

- GST notices and scrutiny

- ITC reversal with interest

- Penalty implications

Therefore, businesses should maintain strong ITC reconciliation practices between purchase records, GSTR-2B, and GSTR-3B to ensure accurate compliance.

Conclusion

The appearance of duplicate ITC entries in October 2024 GSTR-2B, especially related to QRMP suppliers and ISD filings, highlights the importance of careful GST return verification.

With the Invoice Management System (IMS) still in its early stages, taxpayers must exercise extraordinary caution while claiming ITC in GSTR-3B.Rather than relying solely on auto-populated values, businesses should perform detailed reconciliation and validation to avoid duplicate claims and future compliance complications.