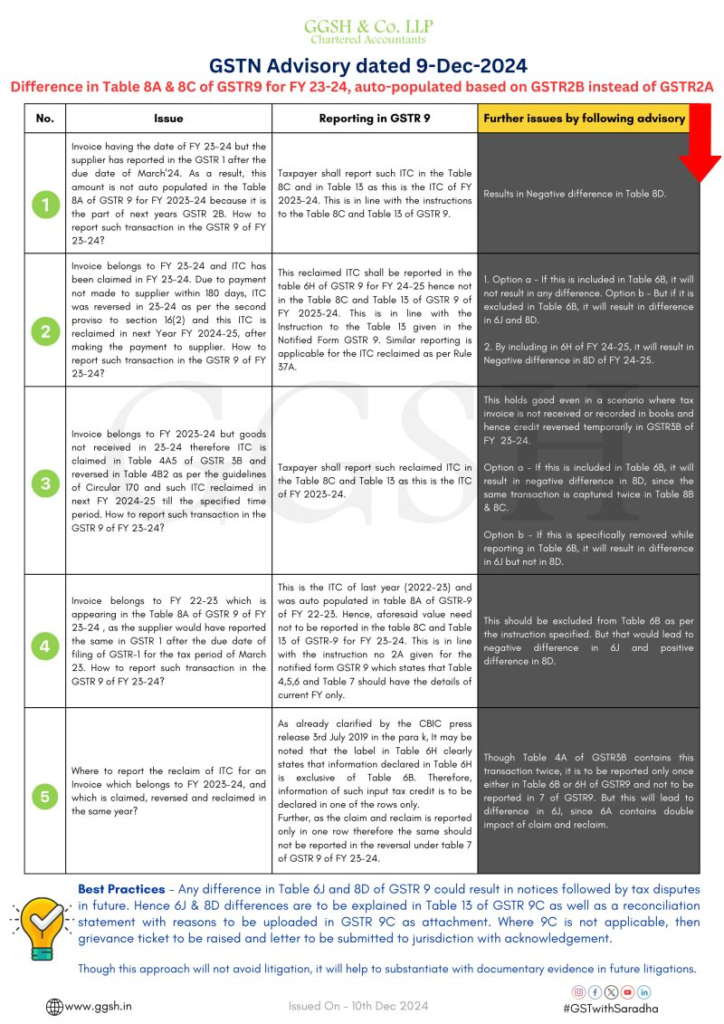

The much-awaited advisory from the Goods and Services Tax Network (GSTN) has been released regarding the difference in values between Table 8A and Table 8C of GSTR-9 Annual Return for FY 2023-24.

For FY 2023-24, Table 8A is auto-populated based on GSTR-2B instead of GSTR-2A, which has created significant reconciliation challenges for taxpayers.

However, instead of offering a complete solution, the advisory appears to create further complexities in reporting. At best, it confirms that GSTN is aware of the challenges in this form, though the suggested approach may still result in differences that could trigger future disputes.

In the attached document, we have also highlighted additional issues and mismatches that may arise while strictly following the advisory instructions.

Practical View on the Advisory

In my view, although the advisory suggestions may lead to differences in the form and potential notices in the future, adopting any alternate approach may place taxpayers in an even more uncertain position.

Therefore, following the advisory may still be the safer approach, as it provides a reasonable explanation for why differences are reported in the return.

It often appears that this form, in a self-assessment tax regime, is structured more for future litigation triggers rather than simple annual reporting.

A complete solution may only be possible if the entire structure of GSTR-9 is redesigned to properly capture all ITC reporting scenarios.

Recommended Best Practice

Any difference between Table 6J and Table 8D of GSTR-9 may potentially result in future notices and tax disputes.

Hence, the following best practice is advisable:

• Differences between Table 6J and Table 8D should be properly explained in Table 13 of GSTR-9C.

• A detailed reconciliation statement with reasons should be prepared and uploaded as an attachment in GSTR-9C.

• Where GSTR-9C is not applicable, taxpayers should:

- Raise a grievance ticket on the GST portal, and

- Submit a formal letter to the jurisdictional officer with acknowledgement.

Important Note

This approach may not completely avoid litigation, but it helps create documentary evidence and justification to defend the differences during future assessments or audits.

Maintaining proper documentation today can significantly help in handling future GST litigation effectively.💬 Views expressed are personal. Comments and professional perspectives are welcome.