India’s GST litigation framework is entering a more structured phase with the introduction of the GST Appellate Tribunal (Procedure) Rules, 2025. These long-awaited rules have been notified by the Government under Section 111 of the Central Goods and Services Tax Act, 2017, laying down a clear procedural roadmap for appeals before the Goods and Services Tax Appellate Tribunal (GSTAT).

The rules mark an important milestone in the evolution of GST dispute resolution in India, bringing standardized procedures, digital integration, and defined hearing protocols to appellate proceedings.

With these procedural guidelines now in place, the GST appellate mechanism is expected to function with greater transparency, efficiency, and consistency across the country.

Effective Date: 24 April 2025

Applicability: All appeals filed before the GST Appellate Tribunal

Why the GST Appellate Tribunal Procedure Rules Matter

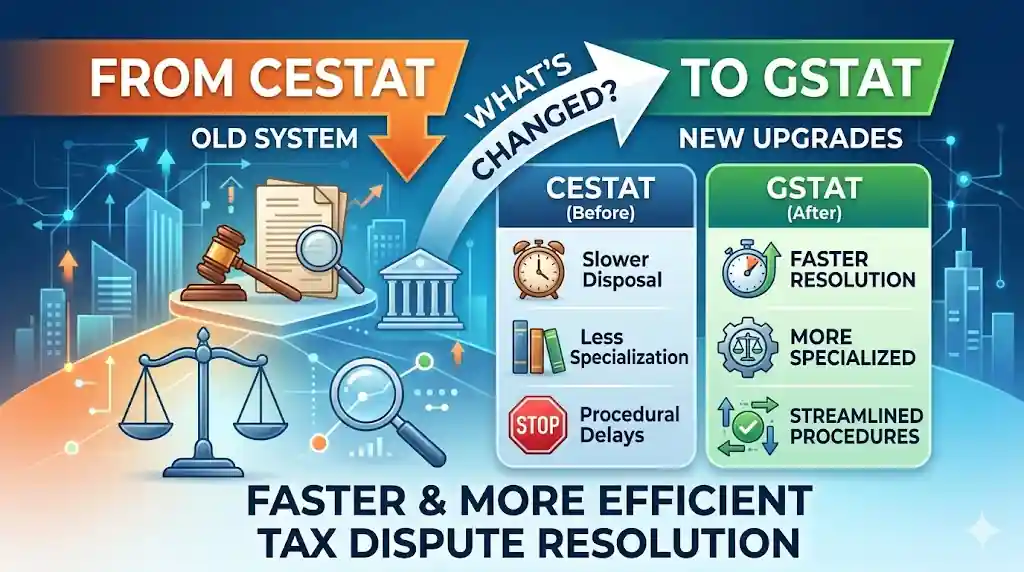

Since the introduction of GST in 2017, the absence of a fully operational appellate tribunal created a gap in the GST litigation hierarchy. Taxpayers often had to approach High Courts directly after decisions from the first appellate authority.

The introduction of the GSTAT procedural rules now completes a critical layer in the dispute resolution system, ensuring that GST appeals follow a structured and uniform process before reaching higher courts.

For businesses, tax professionals, and legal practitioners, these rules provide clarity on:

- Filing procedures for GST appeals

- Documentation requirements

- Hearing protocols and case management

- Administrative powers of the tribunal

This brings much-needed predictability to the GST appeals process in India.

Digital Filing and Technology Integration

One of the key highlights of the GST Appellate Tribunal (Procedure) Rules, 2025 is the emphasis on digital filing and electronic case management.

Appeals before the tribunal are designed to be handled through structured digital processes, which will help:

- Reduce procedural delays

- Improve transparency in documentation

- Enable easier tracking of appeals

- Support efficient case management

Digital systems also ensure better coordination between taxpayers, tax authorities, and the tribunal registry.

Defined Hearing Protocols for GST Appeals

The new procedural rules introduce clear hearing protocols, which help standardize how appeals are heard and adjudicated before the tribunal.

Key procedural aspects include:

- Structured submission of pleadings and documents

- Standardized formatting requirements

- Clear timelines for filing appeals and responses

- Defined roles and powers of the tribunal registry

These measures aim to ensure consistency in appellate proceedings across GSTAT benches.

Improving Transparency in GST Litigation

Another important objective of the new rules is to enhance transparency in GST dispute resolution.

By clearly defining procedural standards, the rules reduce ambiguity in how appeals are processed. This ensures that taxpayers and authorities operate within a uniform procedural framework, minimizing inconsistencies across different benches.

Such transparency is essential for building confidence in the GST appellate system.

Efficiency in Handling GST Disputes

With the introduction of these procedural rules, the GST Appellate Tribunal is expected to handle disputes with greater efficiency and clarity.

Standardized processes help:

- Streamline case management

- Reduce procedural disputes

- Improve the overall pace of litigation

For businesses dealing with GST disputes, this could lead to faster resolution of appeals and reduced uncertainty in tax matters.

A Progressive Step for GST Litigation in India

The notification of the GST Appellate Tribunal (Procedure) Rules, 2025 represents a significant step toward strengthening the GST dispute resolution framework.

By introducing digital processes, defined hearing protocols, and standardized procedures, the Government has moved toward building a more modern and efficient appellate system under GST.As the tribunal begins functioning under these rules from 24 April 2025, taxpayers, businesses, and professionals involved in GST litigation can expect a more structured and predictable appellate process.