A welcome relief for businesses and corporate promoters! The Goods and Services Tax Network (GSTN) has issued an advisory dated 3rd March 2025 bringing an important improvement to the #Biometric #AadhaarAuthentication process for GST registration.

What’s the Key Relief?

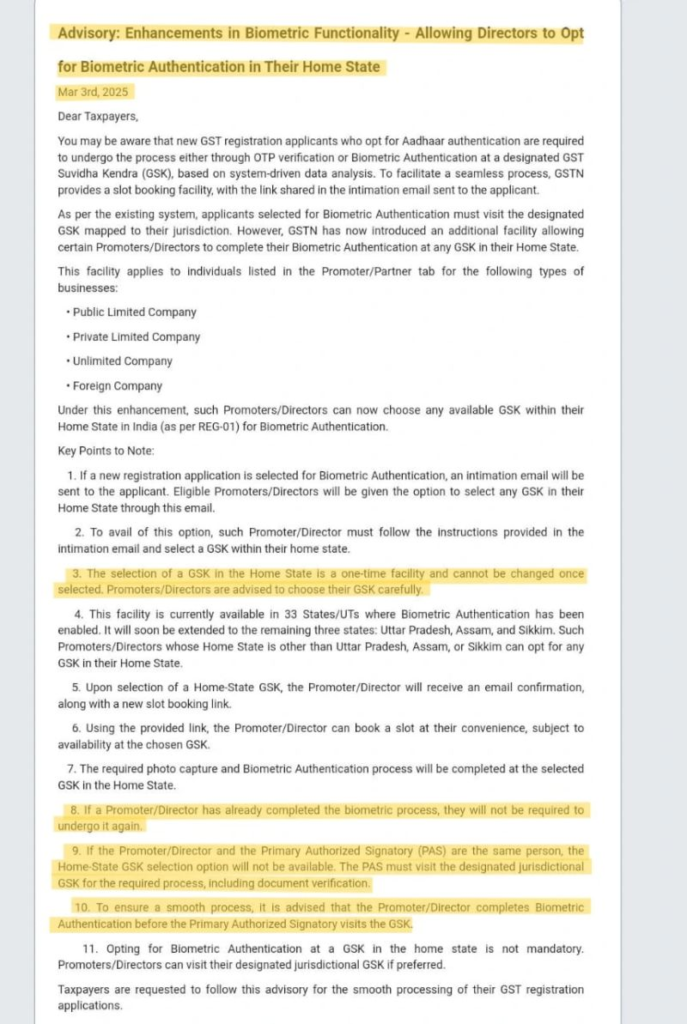

Earlier, Promoters / Partners / Directors of companies often had to travel to multiple states to complete biometric Aadhaar authentication for GST registrations.

✅ Now, only a ONE-TIME biometric authentication in the home state is required.

This change directly addresses a major operational challenge faced by many corporates operating across multiple states.

How the New Process Works

• Promoters / Directors can complete one-time biometric Aadhaar authentication in their home state.

• For registrations in other states, businesses can nominate an Alternate Primary Authorized Signatory (PAS).

• The PAS will complete the biometric authentication locally in the respective state where the GST registration is being processed.

Why This Matters

✔ Eliminates repeated interstate travel for directors

✔ Reduces compliance burden and administrative delays

✔ Improves operational efficiency for multi-state businesses

📄 The advisory issued by Goods and Services Tax Network highlights important details—particularly paragraphs 3, 8, 9, and 10, which taxpayers should carefully review.

This is definitely a progressive step toward simplifying GST registration compliance.

💬 What do you think about this change? Will this make multi-state GST registrations easier for businesses?