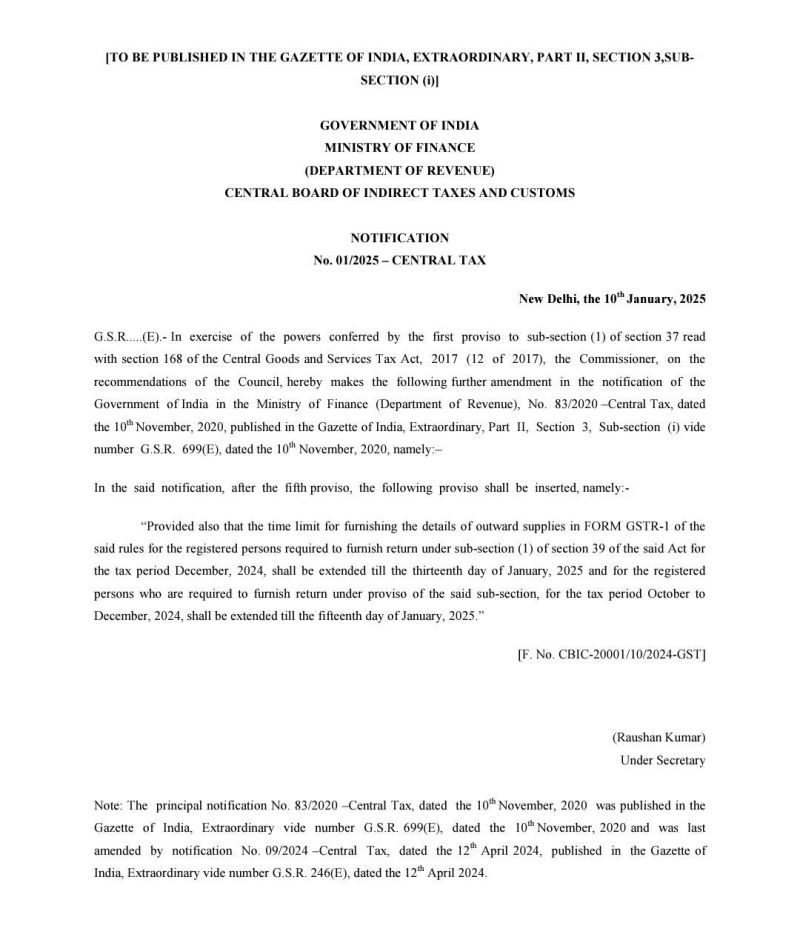

The Goods and Services Tax Network (GSTN) has announced extension of due dates for certain GST returns for the tax period December 2024.

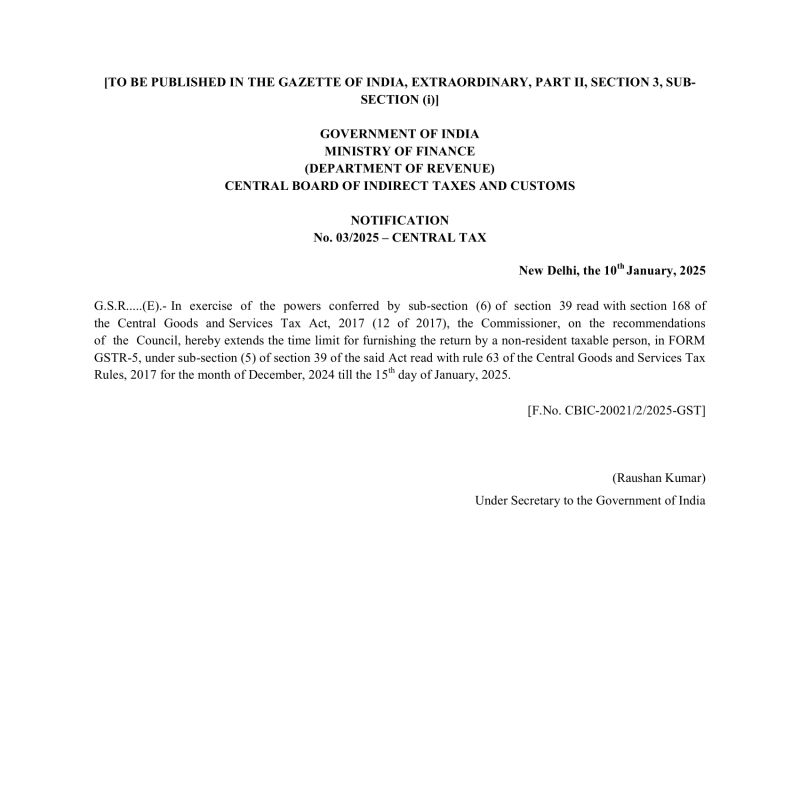

📅 GSTR-5 (Non-Resident Taxable Person Return)

📅 GSTR-6 (Input Service Distributor – ISD)

• Due date extended from 13.01.2025 to 15.01.2025

📅 GSTR-7 (TDS Return)

📅 GSTR-8 (TCS Return)

• Due date extended from 10.01.2025 to 12.01.2025

📌 Taxpayers are advised to utilize the extended timeline to ensure timely and accurate filing of returns to avoid late fees or compliance issues.

Stay updated. Stay compliant. ✅