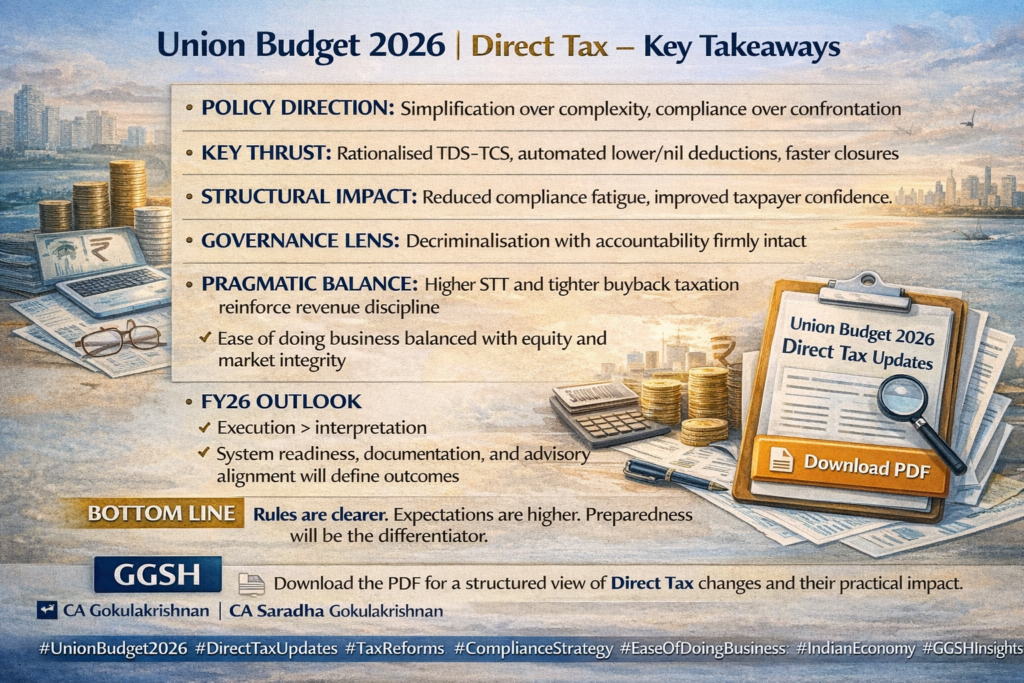

The Union Budget 2026 signals a clear shift in India’s direct tax policy framework. The government appears to be moving toward simplification of tax procedures, technology-driven compliance, and reduced litigation, while maintaining strong accountability mechanisms.

The policy direction reflects a balance between ease of doing business and disciplined tax governance, which will significantly influence how taxpayers, businesses, and professionals manage compliance in FY 2026 and beyond.

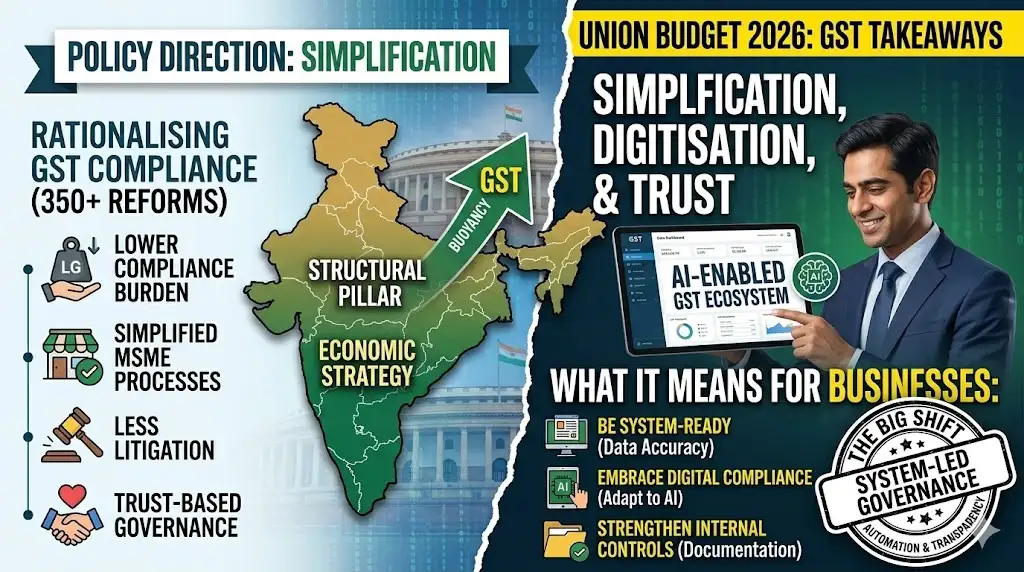

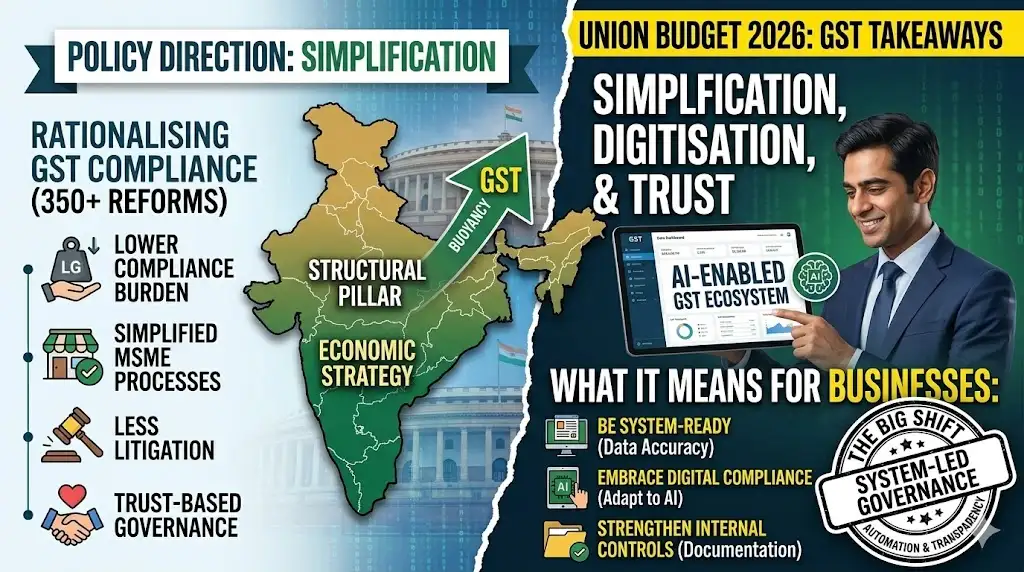

Policy Direction: Simplification Over Complexity

One of the central themes of the Union Budget 2026 direct tax proposals is the move toward simplified tax administration.

The objective is to reduce unnecessary procedural hurdles while encouraging voluntary compliance and transparency.

The reforms are guided by the policy framework set by the Ministry of Finance under the Government of India.

Key emphasis areas include:

- Simplified tax rules

- Reduced litigation and disputes

- Greater reliance on digital systems

- Faster resolution of taxpayer matters

This approach signals a shift from adversarial tax enforcement toward cooperative compliance.

Rationalised TDS and TCS Framework

A major structural reform under the budget involves the rationalisation of TDS (Tax Deducted at Source) and TCS (Tax Collected at Source) provisions.

The reforms aim to:

- Reduce overlapping deduction and collection mechanisms

- Streamline compliance obligations for businesses

- Improve efficiency in tax reporting and credit matching

The initiative is expected to lower administrative burden on taxpayers while strengthening the overall tax credit ecosystem.

Automated Lower or Nil TDS Mechanisms

The budget also highlights increased automation in lower or nil TDS deduction approvals.

Through technology integration with the tax administration system operated by the Central Board of Direct Taxes, taxpayers may experience:

- Faster processing of lower deduction certificate applications

- Reduced manual intervention

- Greater transparency in approval processes

This automation is intended to minimise delays and reduce compliance friction for businesses.

Faster Closure of Tax Matters

Another notable policy direction is the emphasis on speedier closure of tax proceedings and disputes.

This reflects the government’s commitment to:

- Reduce long-pending tax litigation

- Provide certainty to taxpayers

- Improve overall tax administration efficiency

Quicker resolution of tax matters can significantly enhance taxpayer confidence and improve the investment environment.

Decriminalisation with Accountability

The budget also continues the trend toward decriminalisation of certain tax offences.

The objective is to ensure that minor procedural errors do not result in criminal prosecution, while maintaining strict action against serious cases of tax evasion or fraud.

This governance approach focuses on:

- Encouraging voluntary compliance

- Reducing fear-based enforcement

- Maintaining accountability for deliberate violations

Market Discipline Through STT and Buyback Tax Changes

Despite the push toward simplification, the budget also reinforces revenue discipline and market integrity.

Measures such as:

- Higher Securities Transaction Tax (STT)

- Stricter buyback taxation provisions

demonstrate the government’s attempt to maintain equity in capital markets while protecting tax revenues.

These measures influence trading strategies, corporate restructuring, and investor decision-making.

FY 2026 Outlook: Execution Will Matter

For FY 2026, the focus shifts from interpreting tax rules to effectively implementing them.

Success under the new framework will depend on:

- System readiness and digital integration

- Strong documentation practices

- Alignment between businesses and tax advisors

- Timely compliance with updated procedures

Businesses that adapt early to the evolving technology-driven tax environment will have a clear advantage.