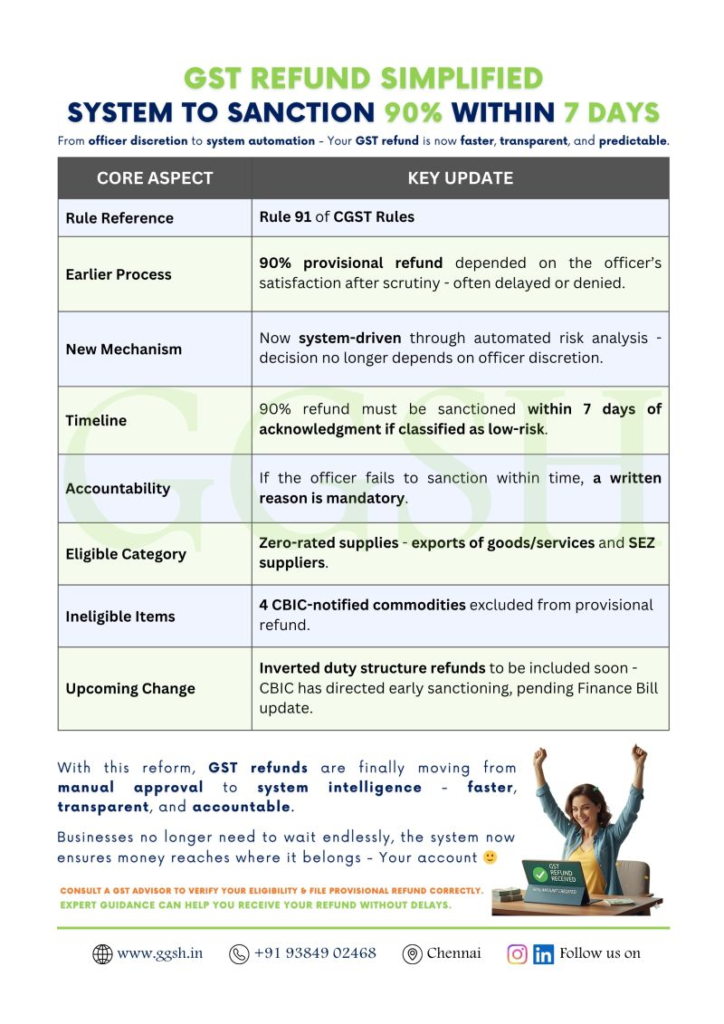

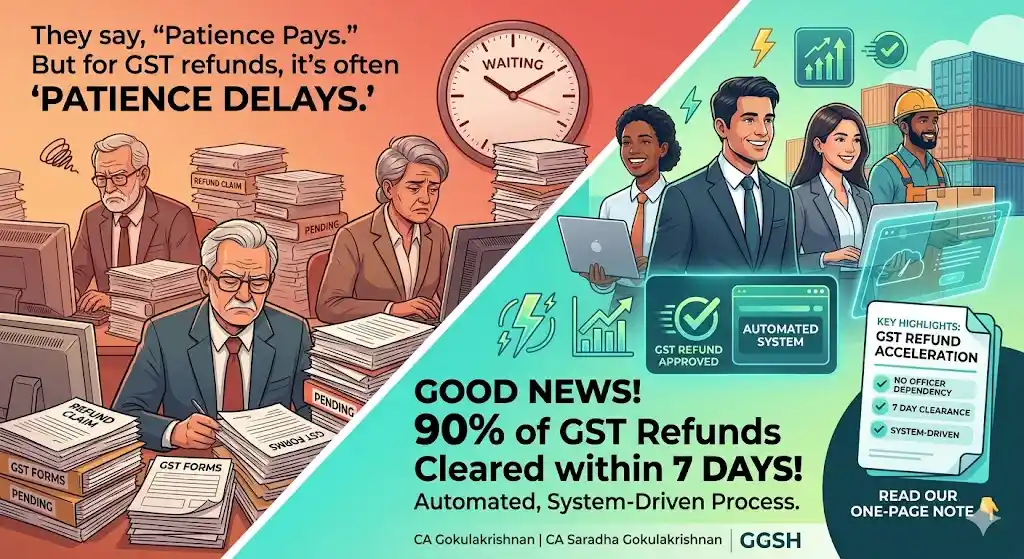

But when it comes to GST refunds, many taxpayers would agree it has often felt more like “Patience delays.”

Now, there’s finally some GOOD NEWS.

The GST refund system is becoming more automated, and nearly 90% of GST refund applications may now be processed within just 7 days.

This shift aims to create a system-driven process with minimal manual intervention.

That means:

✔ Less dependency on officers

✔ Reduced follow-ups and delays

✔ Faster working capital relief for businesses

A welcome development for businesses, exporters, and tax professionals who have long dealt with extended refund timelines.

As automation strengthens the GST ecosystem, refund processing is expected to become more transparent, predictable, and efficient.

We’ve put together a simple one-page note explaining the update and what it means in practice.

Take a moment to read it — it may change how you look at GST refunds.