The Union Budget 2026 signals a decisive continuation of structural economic reforms in India, prioritising long-term competitiveness over short-term populism. Rather than focusing on headline announcements, the government has emphasised policy stability, fiscal discipline, and execution-led governance.

For investors, businesses, and policymakers, the message is clear: predictable policy frameworks and systemic reforms will shape India’s economic trajectory in the coming decade.

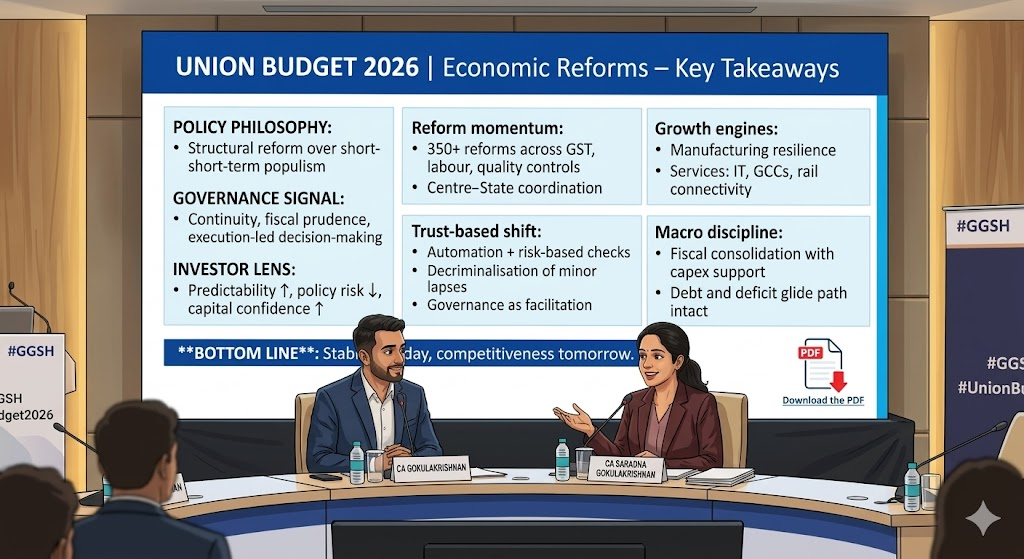

Policy Philosophy: Structural Reform Over Short-Term Populism

A central theme of Union Budget 2026 economic reforms is the commitment to deep structural transformation rather than temporary stimulus measures.

The policy direction aligns with the broader economic strategy of the Government of India and is implemented through the Ministry of Finance.

This philosophy focuses on:

- Strengthening institutional frameworks

- Enhancing regulatory clarity

- Promoting sustainable economic growth

- Ensuring long-term macroeconomic stability

Such an approach is designed to build investor confidence while improving the overall business environment in India.

Governance Signal: Continuity and Fiscal Prudence

The budget reinforces the government’s commitment to policy continuity and fiscal prudence.

In recent years, India’s economic policy has increasingly moved toward execution-driven governance, where reforms are implemented gradually but consistently.

Key governance priorities include:

- Maintaining a disciplined fiscal framework

- Strengthening institutional capacity

- Ensuring predictable regulatory environments

- Improving efficiency in policy implementation

For global investors and domestic businesses alike, policy consistency reduces uncertainty and lowers regulatory risk.

Investor Perspective: Predictability and Confidence

One of the most important outcomes of the reform-oriented approach is the increase in investor confidence.

Stable policy frameworks create a favourable environment for:

- Domestic investment

- Foreign direct investment (FDI)

- Long-term infrastructure financing

- Capital market participation

When investors perceive lower policy risk and higher regulatory predictability, capital flows tend to increase, strengthening the broader economic ecosystem.

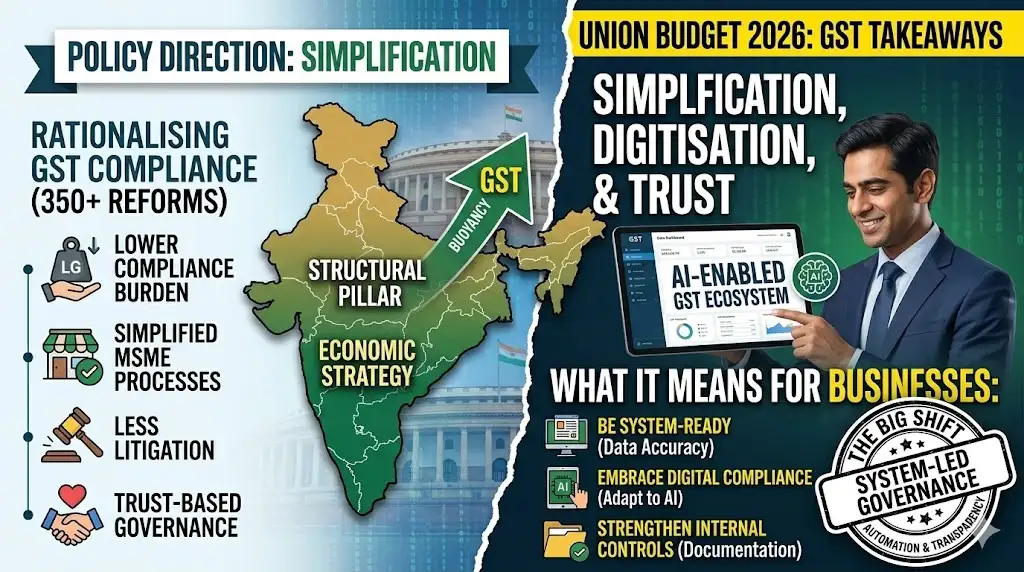

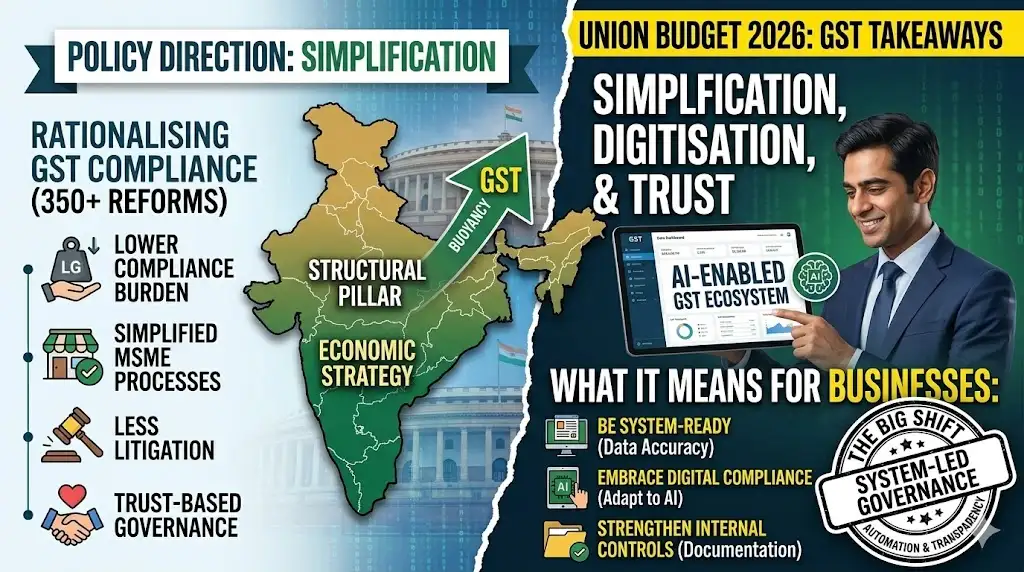

Reform Momentum: 350+ Structural Improvements

India’s reform momentum continues with more than 350 policy and regulatory improvements implemented across multiple sectors.

These reforms cover areas such as:

- Tax administration and GST processes

- Labour law rationalisation

- Quality control standards in manufacturing

- Digital governance systems

Many of these reforms are implemented through cooperation between the central government and state governments, guided by policy coordination bodies such as the GST Council.

This Centre–State collaboration plays a crucial role in ensuring that reform initiatives translate into real economic outcomes.

Shift Toward Trust-Based Governance

Another key feature of the reform strategy is the transition toward trust-based governance models.

Instead of heavy procedural control, the government is adopting technology-driven monitoring systems combined with risk-based compliance checks.

Key elements of this approach include:

- Increased automation in regulatory systems

- Risk-based verification mechanisms

- Decriminalisation of minor procedural lapses

- Reduced reliance on manual intervention

These measures are designed to shift governance from control-oriented administration to facilitation-oriented regulation.

Growth Engines: Manufacturing and Services

The budget also highlights the importance of strengthening India’s core economic growth engines.

Manufacturing Expansion

India’s manufacturing strategy focuses on:

- Building resilient supply chains

- Deepening domestic value chains

- Improving quality standards

- Enhancing export competitiveness

Manufacturing growth supports employment generation and strengthens India’s position in global supply networks.

Services Sector Multipliers

Alongside manufacturing, the services sector continues to play a crucial role in economic expansion.

High-growth segments include:

- Information technology services

- Global Capability Centres (GCCs)

- Data and digital infrastructure

- Rail connectivity and logistics services

Together, these sectors act as multipliers for productivity and economic growth.

Macro Discipline: Fiscal Consolidation with Growth Support

The budget maintains a strong focus on fiscal discipline while supporting economic growth through capital expenditure.

The fiscal strategy aims to:

- Maintain a stable debt-to-GDP trajectory

- Follow a clear deficit reduction glide path

- Continue strategic public infrastructure investment

This balanced approach ensures that economic expansion is supported without compromising fiscal sustainability.

Why These Reforms Matter for Businesses

For businesses operating in India, the economic reforms outlined in Union Budget 2026 bring several important implications:

- Greater regulatory clarity

- Improved ease of doing business

- Stronger digital governance systems

- Increased investment opportunities

Companies that align with the evolving policy environment, compliance frameworks, and digital systems will be better positioned to benefit from India’s growth trajectory.

Bottom Line

The Union Budget 2026 economic reform strategy is not about short-term announcements but about systemic transformation of the Indian economy.

The focus is clear:

- Structural reform instead of temporary policy measures

- Stable governance frameworks

- Sustainable fiscal management

- Long-term competitiveness

In essence, the budget reflects reform by design rather than reform by declaration.The outcome is a policy environment aimed at delivering stability today and stronger economic competitiveness tomorrow.