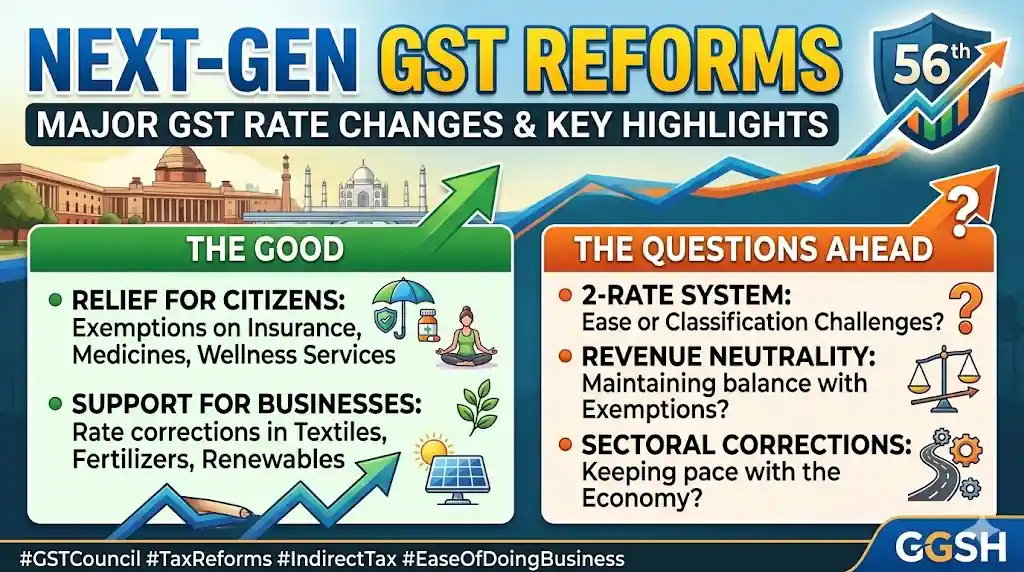

India’s indirect tax landscape is moving toward a simpler and more streamlined Goods and Services Tax (GST) system. Major policy updates were discussed during the 56th meeting of the GST Council, held on 03 September 2025 in New Delhi.

The meeting of the GST Council marks an important step toward next-generation GST reforms, focusing on tax simplification, rate rationalisation, and sector-specific relief measures.

Announced as part of a broader reform vision by Narendra Modi, these policy updates aim to make the GST framework citizen-centric, business-friendly, and growth-oriented.

The proposed reforms signal the government’s continued commitment to building a predictable, transparent, and future-ready indirect tax regime in India.

Key Highlights of the 56th GST Council Meeting

The latest GST Council meeting introduced several proposals focused on tax relief, industry support, and structural simplification of GST rates.

Relief Measures for Citizens

One of the central themes of the reforms is providing tax relief for individuals and essential services.

Key proposals include:

- GST exemptions or relief for health insurance services

- Tax relief on lifesaving medicines

- Concessions for wellness and healthcare-related services

These measures are designed to reduce the financial burden on households and improve access to critical healthcare services.

Support for Key Business Sectors

The reforms also aim to strengthen industries by introducing GST rate corrections in important sectors of the economy, including:

- Textiles sector

- Fertilizer industry

- Renewable energy sector

Such adjustments are expected to enhance competitiveness, supply chain efficiency, and investment attractiveness in these sectors.

By recalibrating GST rates, policymakers are attempting to balance revenue collection with economic growth objectives.

GST Rate Rationalisation: Moving Toward a Two-Rate Structure

One of the most discussed proposals is the possibility of transitioning toward a two-rate GST structure.

Currently, India’s GST system includes multiple tax slabs such as:

- 5%

- 12%

- 18%

- 28%

A simplified two-rate GST model could significantly reduce classification disputes, compliance complexity, and administrative challenges.

However, tax experts and industry stakeholders are closely evaluating the practical implications of such a structural change.

Key Questions Surrounding the Proposed GST Reforms

While the reform proposals are widely seen as a positive development, several important questions remain.

1. Will a Two-Rate GST System Simplify Compliance?

A reduced number of tax slabs may simplify compliance for businesses. However, classification disputes between categories of goods and services could still arise, requiring clearer guidelines.

2. How Will Revenue Neutrality Be Maintained?

Expanding exemptions and lowering rates in certain sectors raises concerns about maintaining government tax revenues while ensuring fiscal stability.

Policymakers will need to carefully design the new tax structure to ensure revenue neutrality while supporting economic growth.

3. Can GST Reforms Keep Pace with the Evolving Economy?

India’s economy is rapidly evolving, with digital services, renewable energy, and new industries emerging quickly.

Regular sector-specific updates may be necessary to ensure the GST framework remains adaptive, competitive, and aligned with modern economic trends.

Why These GST Reforms Matter for Businesses

For businesses, especially those dealing with GST compliance, tax planning, and supply chain management, these reforms could have significant implications.

Potential benefits include:

- Simplified GST compliance procedures

- Reduced tax classification disputes

- Improved cost predictability

- Enhanced investment environment

However, successful implementation will require clear government guidelines, consistent interpretation, and effective stakeholder engagement.

Expert Perspective: Implementation Will Be Key

While the announcements from the 56th GST Council meeting represent an important policy inflection point, the real impact will depend on how effectively these reforms are implemented.

A successful rollout will require:

- Clear sector-specific guidance

- Smooth transition mechanisms for businesses

- Continuous policy review and stakeholder consultation

With proper execution, these reforms could strengthen India’s GST ecosystem and improve the ease of doing business.

Final Thoughts

India’s next-generation GST reforms represent a major step toward building a simpler, more predictable, and growth-focused indirect tax system.

As businesses, tax professionals, and policymakers analyze the details of these proposals, the coming months will be crucial in determining how these reforms reshape the GST landscape in India.Stakeholder participation and ongoing policy review will be essential to ensure that the GST system continues to evolve alongside the changing needs of the economy.