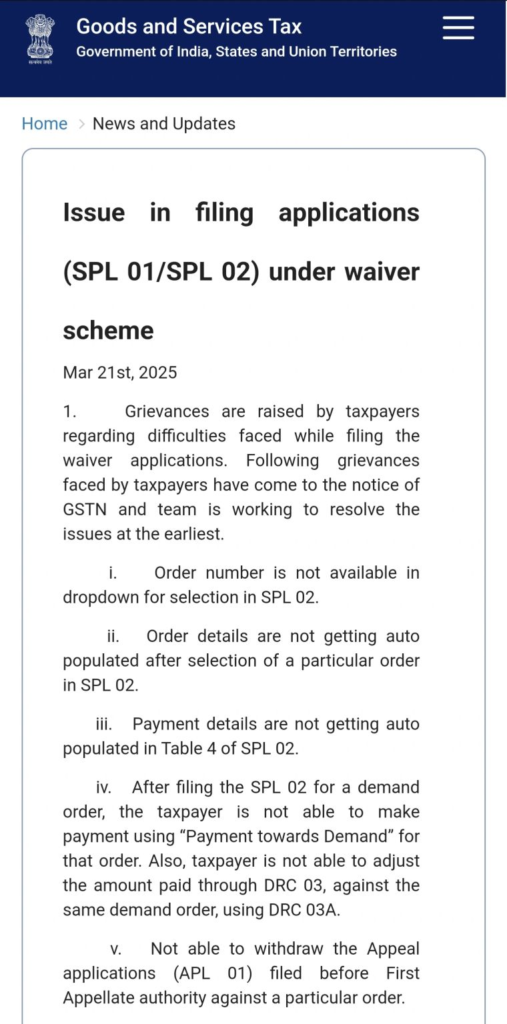

The Goods and Services Tax Network (GSTN) has issued an advisory regarding filing of the SPL application form under the GST Amnesty Scheme.

Here are the key takeaways—keeping it short and simple:

🔍 Key Clarification

1️⃣ 31st March 2025 is the cut-off date only for payment of full tax liability to become eligible under the amnesty scheme.

It is NOT the last date for filing the SPL application form.

2️⃣ Taxpayers facing portal-related issues while filing the SPL form need not panic.

The GSTN technical team is currently working on resolving these portal challenges.

✅ This clarification provides much-needed relief to taxpayers who were concerned about missing the deadline due to technical glitches.

📄 You can check the detailed advisory here:

https://lnkd.in/ggAWibQE

#GST #GSTAmnestyScheme #GSTUpdate #GSTN #TaxCompliance