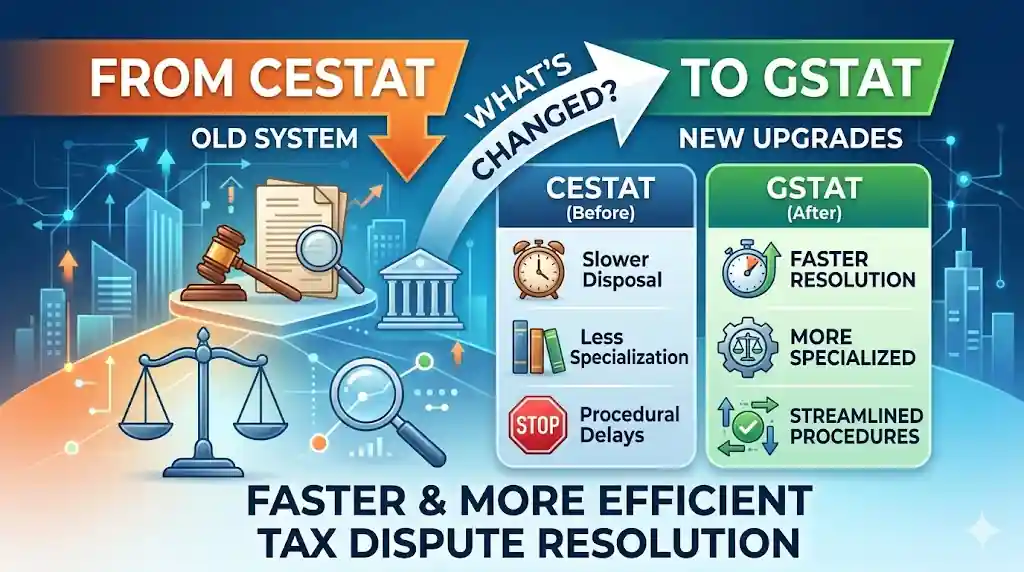

India’s GST framework continues to evolve with a strong focus on improving tax litigation and dispute resolution mechanisms. A major step in this direction is the introduction of the GST Appellate Tribunal (Procedure) Rules, 2025, notified under Section 111 of the CGST Act.

These rules mark a significant shift toward a more structured, transparent, and efficient GST litigation system in India.

Introduction to GSTAT Procedure Rules, 2025

The Government of India has rolled out the much-awaited procedural framework governing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT).

Key Details at a Glance

- Effective Date: 24th April 2025

- Applicability: All appeals filed before GSTAT

- Legal Basis: Section 111 of the CGST Act

These rules are designed to bring consistency and clarity to appellate proceedings under GST.

Key Objectives of GSTAT Procedure Rules, 2025

The newly introduced rules aim to:

- Streamline GST dispute resolution processes

- Introduce uniform procedures across all GSTAT benches

- Enhance transparency in hearings and case handling

- Reduce delays in litigation

- Promote digitalization and efficiency

Major Highlights of GST Appellate Tribunal Rules

1. Digital Filing of Appeals

A major reform under the new rules is the push toward electronic filing (e-filing) of appeals.

- Minimizes paperwork

- Enables faster submission and processing

- Improves accessibility for taxpayers and professionals

2. Defined Hearing Protocols

The rules introduce clear procedures for hearings, ensuring:

- Structured case presentation

- Better time management

- Reduced adjournments

This brings more discipline and predictability to GST litigation.

3. Transparency in Case Management

From filing to final order, the process is now more transparent with:

- Proper documentation flow

- Clear communication of case status

- Reduced scope for ambiguity

4. Standardized Cause Lists and Proceedings

The introduction of organized cause lists ensures:

- Better scheduling of cases

- Improved tracking of hearings

- Efficient tribunal functioning

5. Consistency Across Benches

Uniform procedural rules across all GSTAT benches help ensure:

- Consistent legal interpretation

- Reduced jurisdictional disparities

- Greater confidence among taxpayers

Impact on GST Litigation in India

The GSTAT Procedure Rules, 2025 are expected to significantly improve:

- Speed of dispute resolution

- Ease of filing and tracking appeals

- Transparency in tribunal proceedings

- Reduced litigation backlog

This reform benefits:

- Businesses involved in GST disputes

- Chartered accountants and tax consultants

- Legal professionals handling indirect taxes

- Corporates managing tax risks

A Progressive Step in GST Reform

The introduction of these rules reflects the government’s commitment to strengthening the GST ecosystem in India. By focusing on digitalization, structure, and efficiency, the GST Appellate Tribunal is set to redefine how tax disputes are handled.

Conclusion

The GST Appellate Tribunal (Procedure) Rules, 2025 represent a major milestone in India’s journey toward a modern and efficient tax litigation system.

With clearer procedures, digital processes, and standardized practices, GSTAT is poised to deliver faster and more reliable dispute resolution — a crucial factor in improving the ease of doing business in India.

Share Your Thoughts 💬

Do you think these new GSTAT rules will transform GST litigation in India?

Join the conversation and let us know your views!